Can paying your rent improve your credit score?

I noticed a recent uptick in services that promise to help renters build credit by reporting their rent payments to credit bureaus. Borrowell RentAdvantage is one of them. Instead of your rent payments disappearing into the void every month, they get added to your Equifax credit report alongside other payment history like credit cards or phone bills.

It sounded like a pretty good deal. If I was already paying rent every month, why not have those payments count toward my credit history too?

So I decided to test it myself.

I signed up for Borrowell RentAdvantage, paid for the service, added two years of rent history, and waited 30 days to see whether my credit score would actually change.

Improve your credit score with a Neo Secured Mastercard! Plus, sign up now via the button below and get a $60 welcome bonus.

* Limited-time offer. Only valid for new Neo customers who open their first eligible Neo credit product and make a purchase within 90 days.

I was curious, but also a little skeptical. I already had decent credit, and I wasn't thrilled about adding another financial product tied to my credit report unless there was a clear benefit.

Rent reporting also isn't entirely risk-free. While on-time payments could potentially help your credit history, missed or late payments could also impact your score.

Still, I could see why this might appeal to people trying to build credit for the first time, recover after financial difficulties, or eventually qualify for things like a mortgage with bad credit history.

Here's what happened.

How rent reporting works

Rent reporting is pretty simple.

You pay a service like Borrowell RentAdvantage. Then the company verifies your rent payments and reports them to a credit bureau.

In this case, Borrowell reports to Equifax. It does not report to TransUnion.

Most landlords in Canada do not report rent payments automatically, which means your biggest monthly expense usually does not help your credit score unless you use a third-party service like this.

How it started

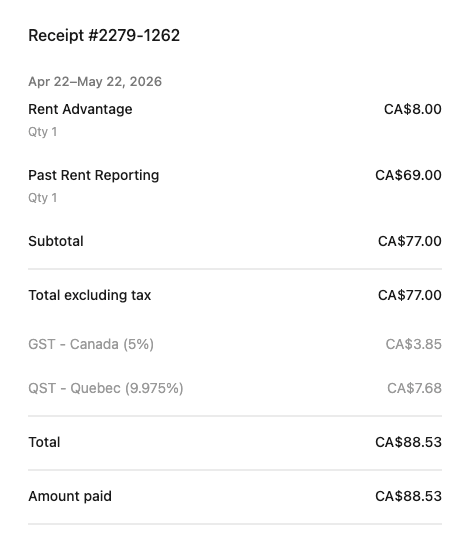

To get started, I created an account with Borrowell. I paid the $8 fee for monthly rent reporting and the $69 fee which allowed me to apply the last two years of my history of rent payments. Total cost for the first month: $88.53.

I uploaded proof of my rent payments (in my case, screenshots of the e-transfers) and connected my bank account so Borrowell could verify the transactions.

About a week later, I got a notification saying my rent history had been added and my credit score had been updated.

But when I checked, nothing had changed. My score was the same, and I could not see my rent anywhere on my credit report.

After reading more about how rent reporting works, I realized this is actually pretty common. Even after Borrowell processes your information, it can take time for the changes to fully appear on your Equifax profile.

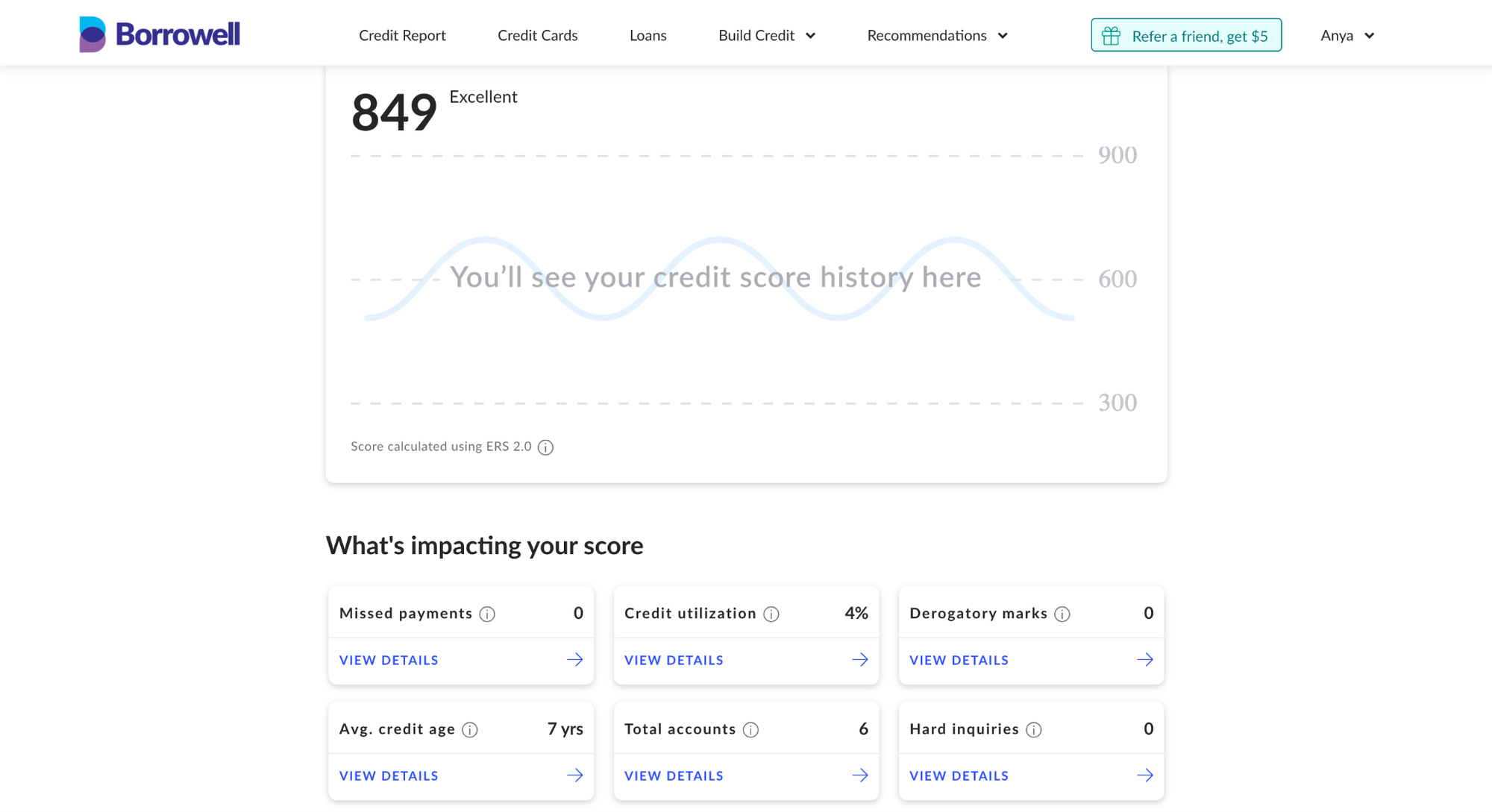

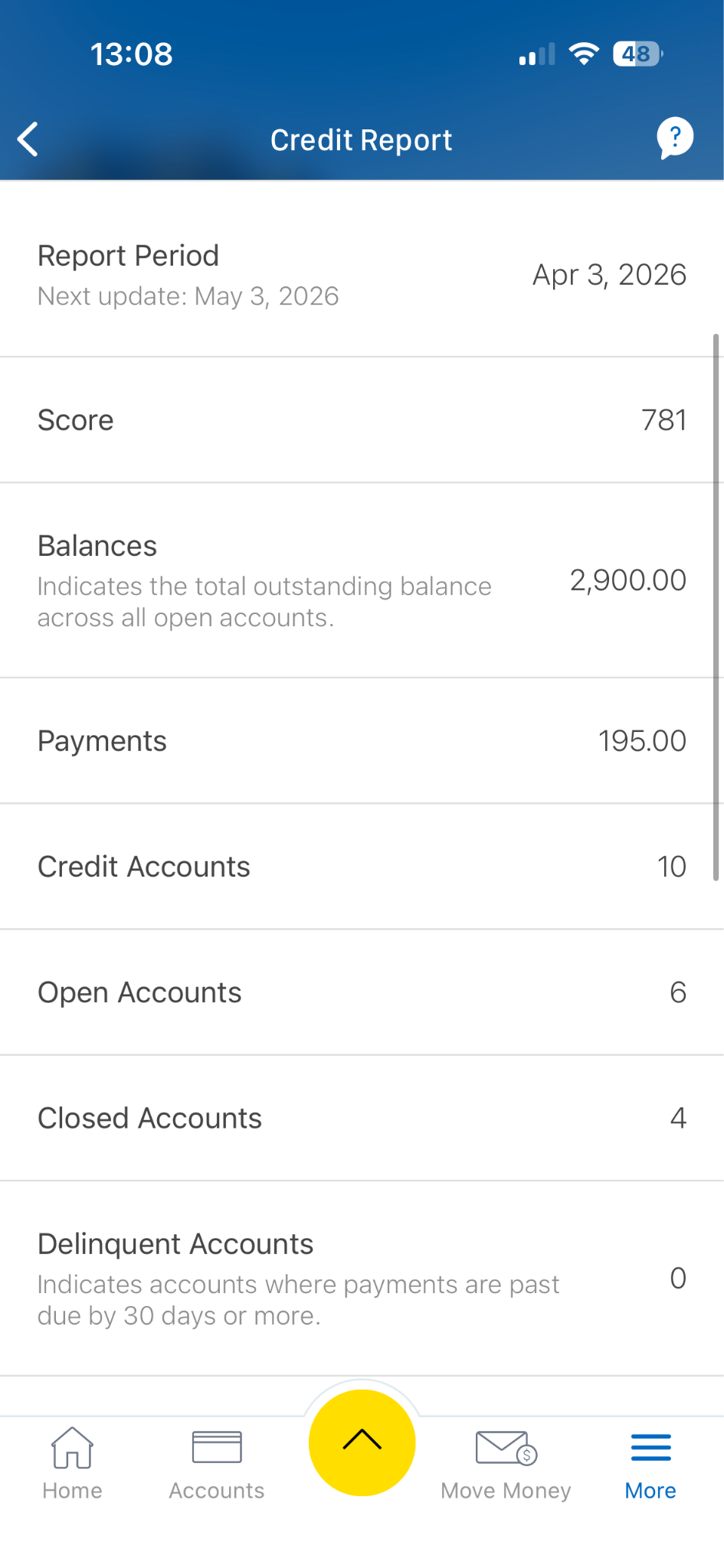

My credit score before using Borrowell RentAdvantage

Before signing up, my scores looked like this:

- Equifax: 849

- TransUnion: 781

That surprised me a bit because I assumed my scores would be much closer together. It turns out credit scores can vary quite a bit between platforms, which is one reason Borrowell and Credit Karma scores may not perfectly match each other even when both are technically accurate.

But it also made this experiment more interesting.

Borrowell RentAdvantage reports to Equifax, not TransUnion. So if rent reporting really works, I should theoretically see movement on the Equifax side only.

What happened after 30 days

After waiting a month, I checked both credit bureaus again.

Here were my results:

- Equifax before: 849

- Equifax after: 849

- TransUnion before: 781

- TransUnion after: 781

So in my case, nothing changed.

My rent history was added, but my scores stayed exactly the same.

Honestly, I was a little disappointed. I thought adding two years of rent history would move the needle at least a bit.

Still, my Equifax score was already extremely high before I started. There may simply not have been much room left for improvement.

Did it actually help my credit score?

For me, it didn’t.

My Equifax score stayed at 849 before and after using Borrowell RentAdvantage. My TransUnion score also stayed the same at 781.

Since I already had years of credit history, active credit cards, and on-time payments, adding rent reporting may not have meaningfully changed how lenders evaluate my profile. There probably just was not much room left for improvement.

If you already have strong credit, paying a monthly fee to report rent may not make much difference. But for renters who are new to Canada, younger people with limited credit history, or anyone rebuilding after financial difficulties, rent reporting could potentially help establish a stronger financial track record.

For example, people struggling to secure traditional rentals due to poor credit sometimes end up relying on cheap motels that rent monthly while trying to get back on their feet.

I also spent some time reading Reddit threads from people who tried rent reporting services themselves. The experiences were mixed. Some people said they saw their score increase after a few months. Others said they noticed little to no difference.

Personally, I still think a regular credit card (or a secured credit card if your credit score is too low) is probably the better option for most people.

My final verdict

After trying Borrowell RentAdvantage myself, I'm left with mixed feelings.

The service technically did what it promised. My rent history was added to Equifax. But in practical terms, it did not improve my credit score at all.

That said, my credit score was already extremely high before I started the experiment. If I had been building credit from scratch or recovering from financial difficulties, the results may have been different.

For someone rebuilding credit or trying to establish credit for the first time, this could still be worth trying. Rent is usually the biggest monthly payment people make, so it makes sense that it should count for something.

Still, I'm not fully convinced the monthly fee is worth it for the average person with an established credit history.

If your goal is improving your credit score, I still think the basics matter most:

- Pay your bills on time

- Keep your credit utilization low

- Avoid missed payments

- Use a credit card responsibly

Those habits will likely have a bigger impact than paying to report your rent.

Script:Can your rent payments count toward your credit score? Apparently, yes. I recently found out about Borrowell RentAdvantage, a service that lets you apply your rent payments towards your credit score.

The idea is pretty simple: instead of your rent payments disappearing into the void every month, they get added to your credit report alongside things like credit cards or phone bills.

So I signed up, paid for the service, added two years of rent history, and waited to see whether it would make any difference.

Honestly? Not really.

For me, it didn’t seem to move the needle much at all. My Equifax score started at 849 and at the end of the experiment my score was… 849.

That said, I already had pretty established credit, so I could still see this being more useful for newcomers to Canada, younger renters, or people rebuilding after financial difficulties.

I also learned that rent reporting isn’t completely risk-free. If your rent gets reported, missed payments could potentially show up too.

Overall, I’m still a little skeptical about paying for a service to boost your credit score, but I could see it being a helpful tool for people without much established credit or who are trying to rebuild.