Destroying your credit is easy to do. You barely have to try. Rebuilding it is a different story altogether. There are a few different paths, but they all will inevitably lead you to a secured credit card.

Secured credit cards exist because, at some point, the regular system decided you were too risky. Maybe you lost a job. Maybe an emergency wiped out your margin. The reason doesn't matter.

It’s a simple system. Pay a deposit, they hold it and you borrow against your own money. You have to pay interest, of course. In exchange, each on-time payment gets reported to the credit bureaus, and slowly, your score recovers.

It's one of the fastest ways to rebuild credit in Canada. At least, it's supposed to be. I spent several months trying to figure out the best secured credit card in Canada.

Improve your credit score with a Neo Secured Mastercard! Plus, sign up now via the button below and get a $60 welcome bonus.

* Limited-time offer. Only valid for new Neo customers who open their first eligible Neo credit product and make a purchase within 90 days.

The Three Cards At A Glance

The three cards I tested for this were the Home Trust Secured Visa Card, the Neo Secured Mastercard and the Capital One Guaranteed Secured Mastercard. Preliminary research showed some key difference between the cards.

Home Trust lets you trade an annual fee for a lower, fixed interest rate. Neo uses a risk‑based interest range and charges a separate monthly fee to use their app‑driven ecosystem, which can be waived depending on your broader relationship with the company.

*Neo's $7.99/mo Build membership fee is waived if you keep $5,000 or more across your Neo Everyday, Neo Savings, or Neo High-Interest Savings accounts or if you hold the other Neo Mastercard products.

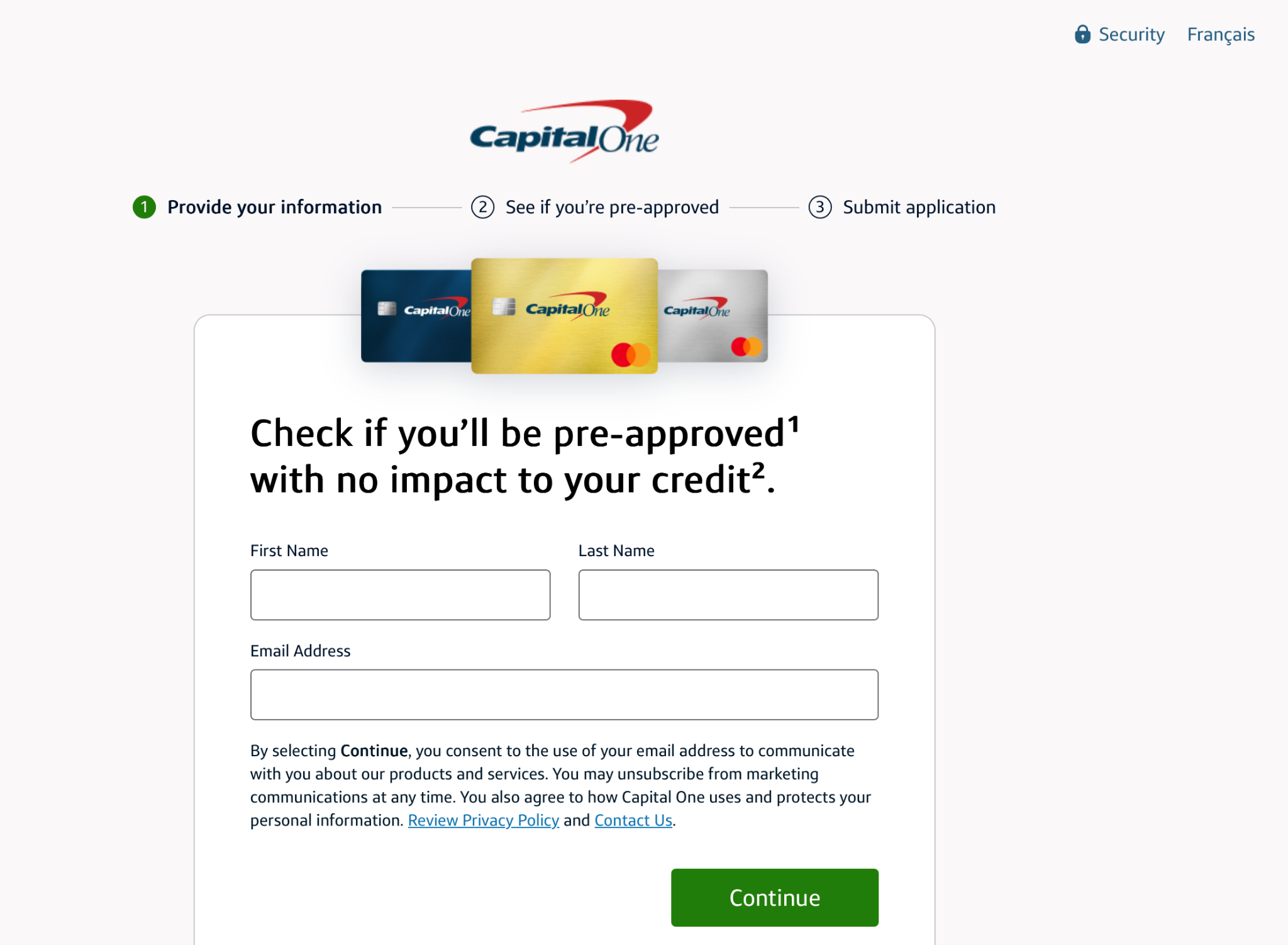

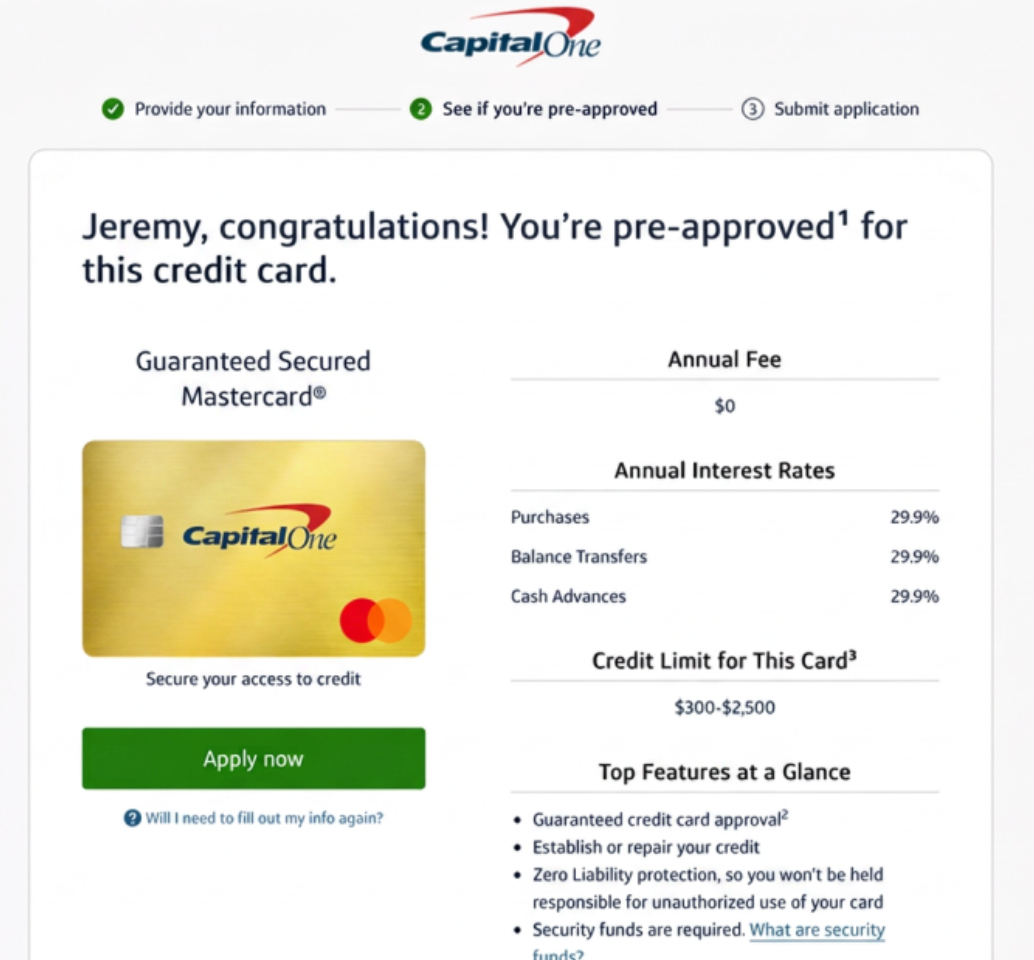

Capital One: Boring, Efficient, Nothing to Report

This is as straightforward as it gets. I applied online. They did a hard credit check. I put down $75 for a $75 limit and had a virtual card ready to use within minutes. The whole thing takes maybe fifteen minutes, if you read it over twice.

I bought a tank of gas, the transaction was posted a day later. It works exactly as advertised.

A physical card arrived in the mail roughly a week later. (photo of Capital One Card)

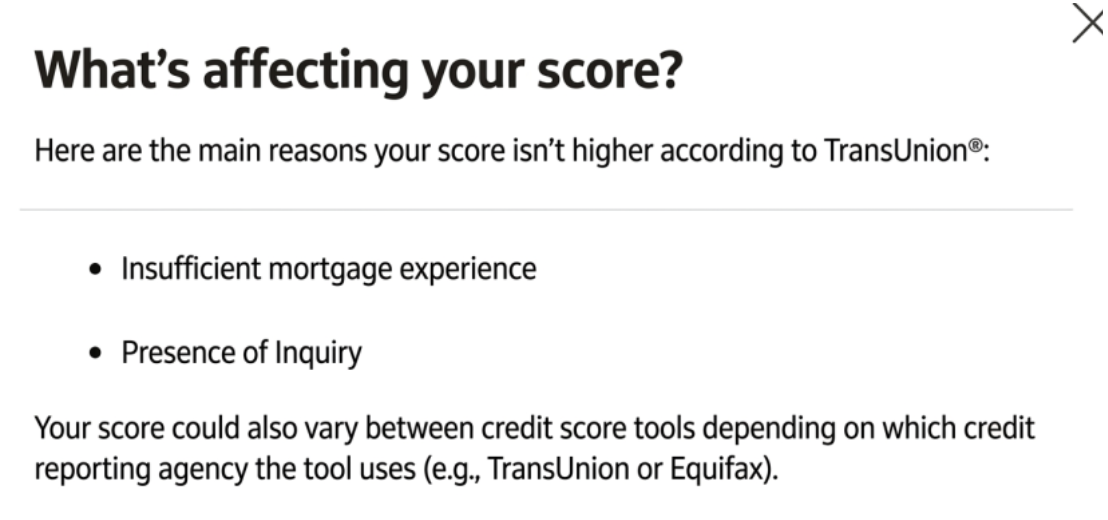

The value beyond the basics comes from Credit Keeper, their free credit-score monitoring built into the card.

There’s no membership tier required. It tracks your score through TransUnion, and surfaces factors affecting it like payment history and credit utilization. Having ease of access to that information is worthwhile, especially if you’re in active rebuild mode.

Verdict: Apply here first. It’s the path of least resistance.

Neo: Affordable, Quick & Decent Cashback

Neo’s Secured Mastercard was similar in most ways. Apply online, hard credit check, and a smaller deposit of $50. The first time I went through the process, there were some issues with the identity confirmation process, and I had to turn my head for the camera a few times before it cleared. There was also a login error that kept me out of my account for a day.

Once I was, everything was very much the same as Capital One. The physical card took about 2 weeks to arrive. Neo has the lowest deposit of the three, which matters when you’re rebuilding on a tight budget.

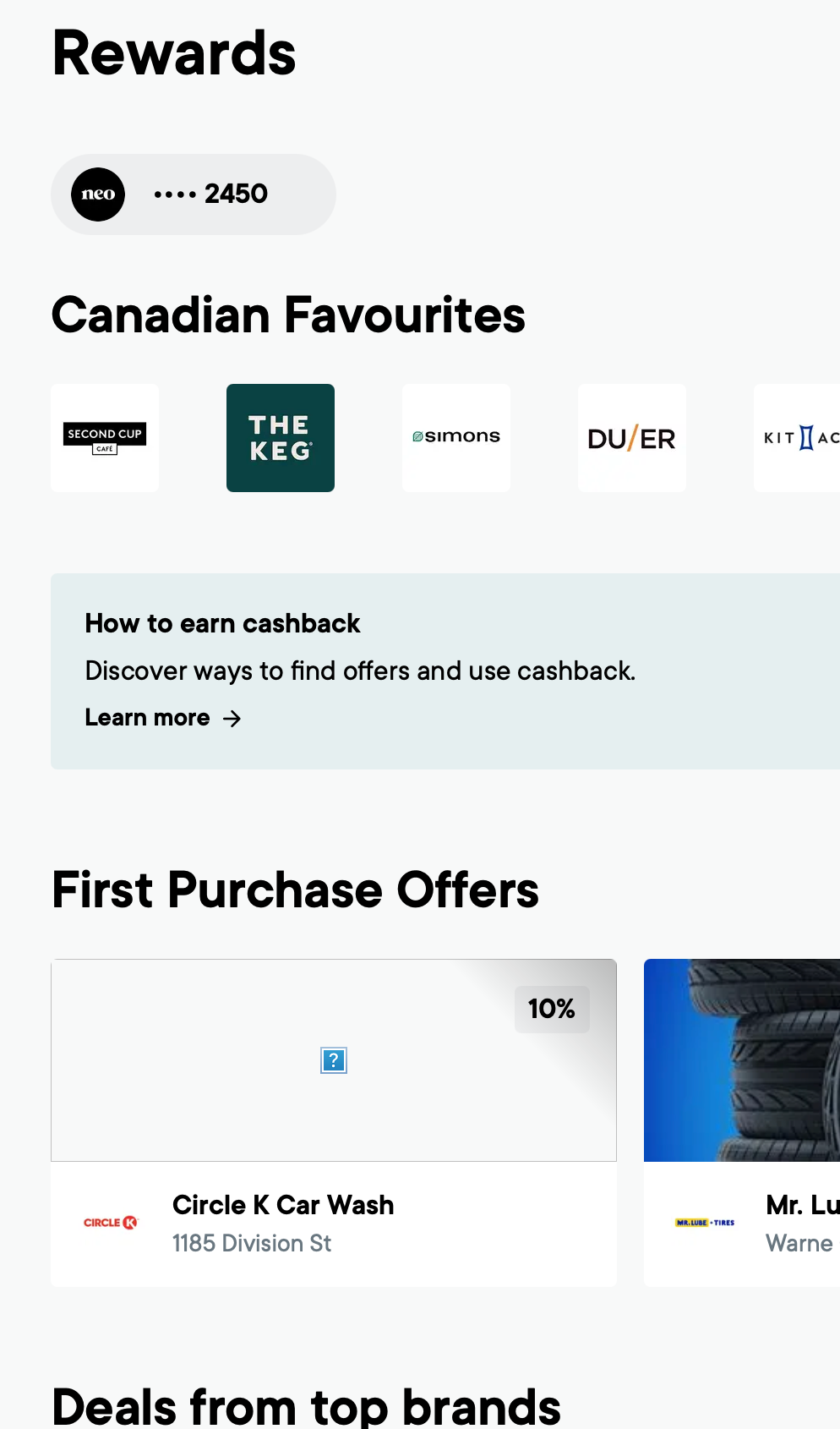

Where Neo stands out is the ecosystem. The card requires a Build membership with Neo for $7.99/mo. It’s similar to Capital One’s Credit Keeper, but promises a more guided experience. The app presents clear milestones and offers tips and coaching to help build your credit faster.

Neo's Build membership also gets you a variety of bells and whistles through their app. You get 1% cashback from any gas & grocery purchases, and special offers from partner brands such as Second Cup, The Keg, and Simons.

Verdict: Best if you care about getting some cashback on your spending or if you need a low deposit floor.

Home Trust: A Case Study in Institutional Failure

Home Trust's interest rate is the lowest of the three (14.90% on the low end).

On paper, it's the best deal. In practice, you may not be able to get it.

The first thing to note is that Home Trust requires a $500 deposit. Not extreme, but certainly a barrier if money is tight.

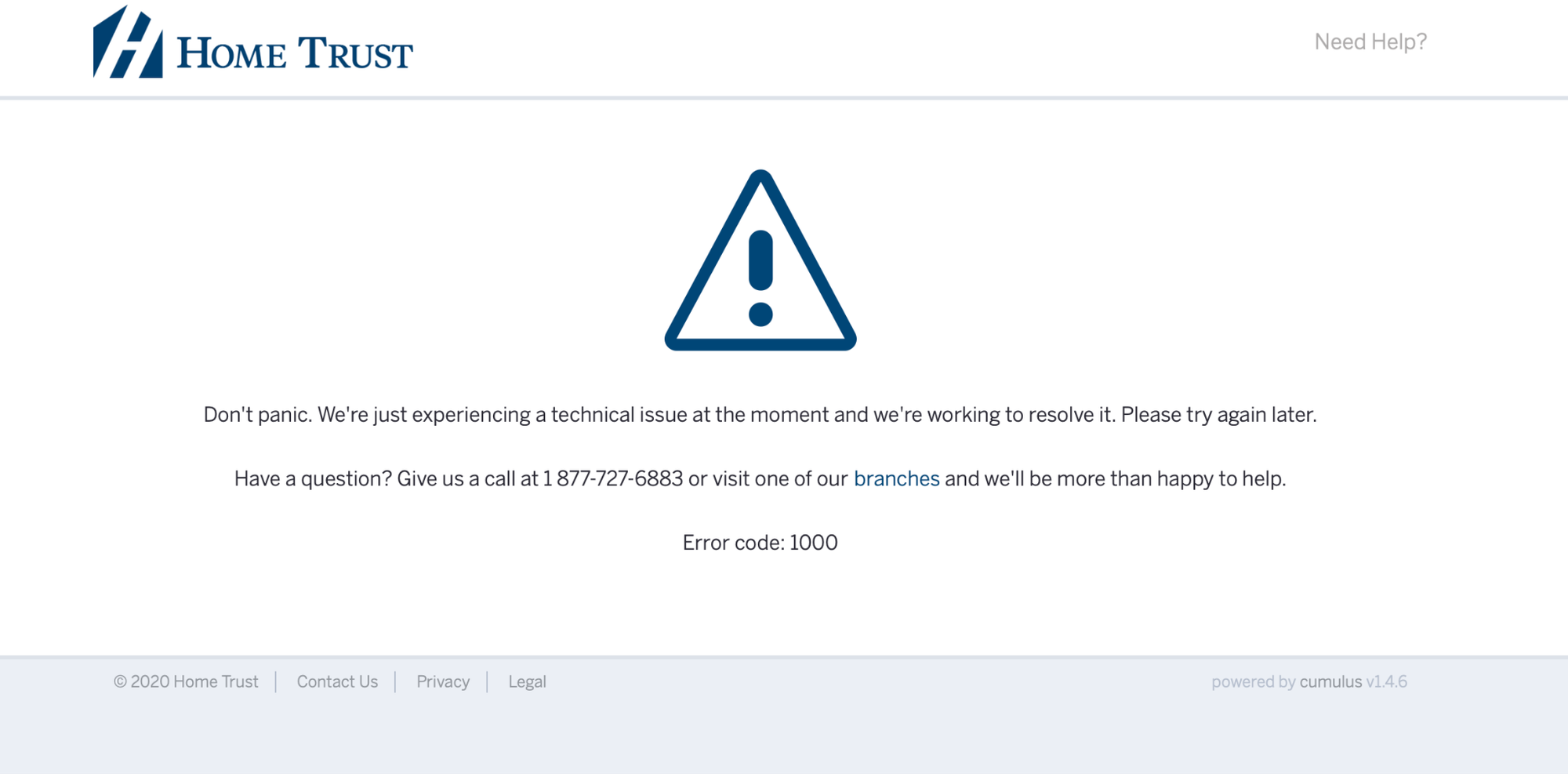

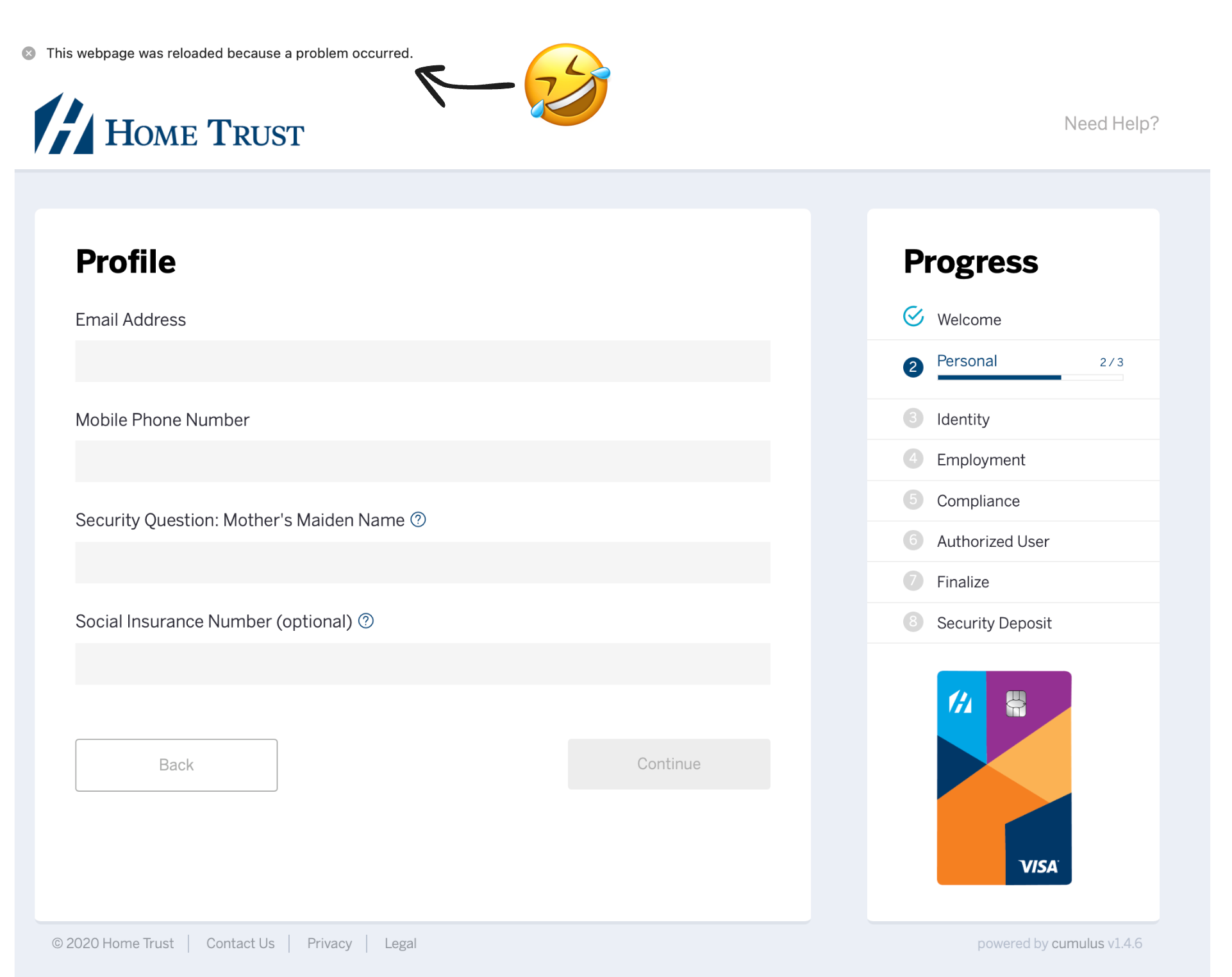

The second thing to note is that their application portal has a problem. Maybe a few problems.

My first few attempts ended up with server errors. Eventually the code changed to 403 errors. I looked up what a 403 error means. "Forbidden." The server understood my request and refused it.

I had gotten myself entirely locked out of the application system. The portal flagged my IP address. The page still won’t load on my home wifi. From then on I had to tether to my mobile data to access the application.

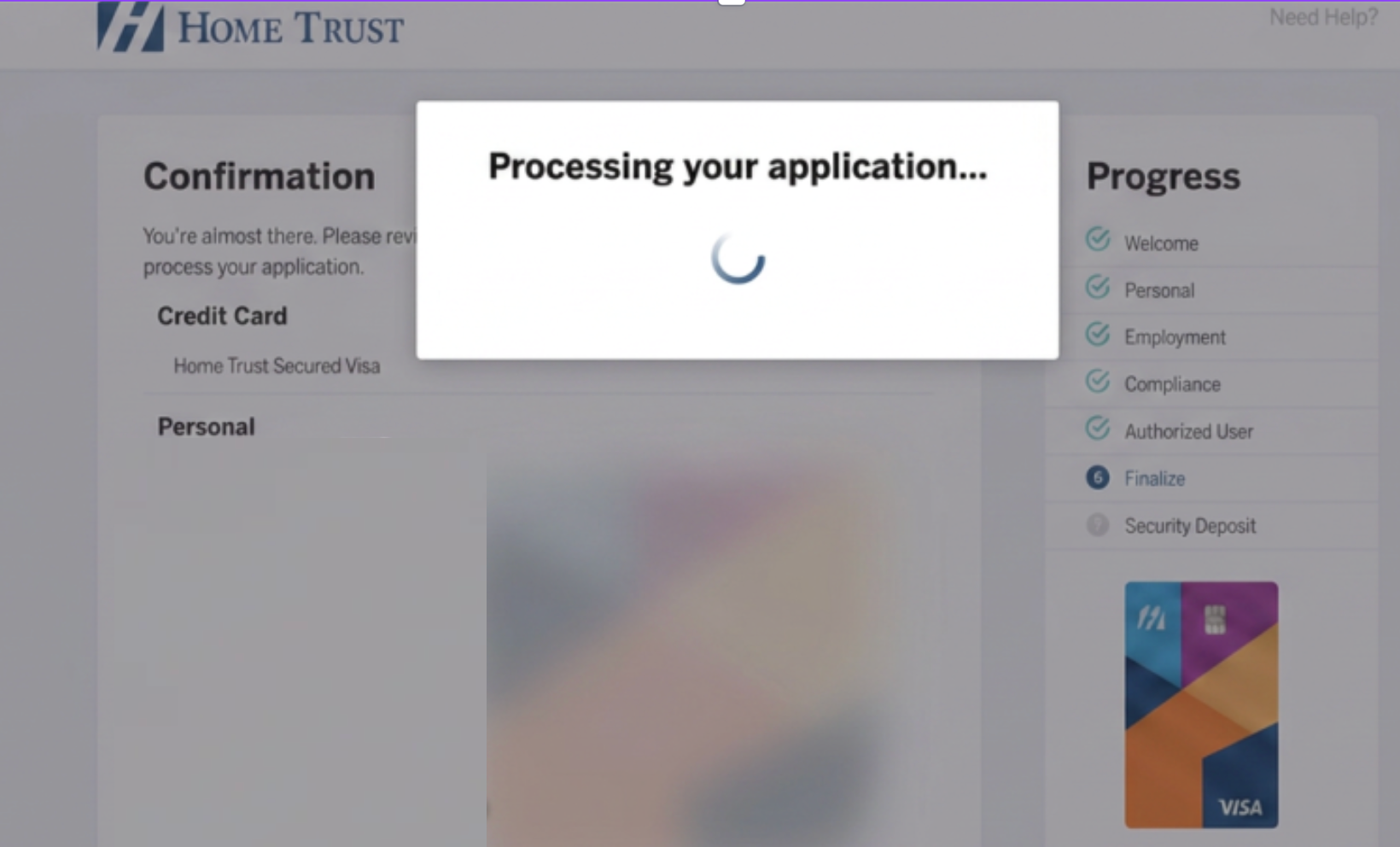

Only once did I make it all the way to the deposit step. The confirmation screen showed all my details, the progress bar was sitting on finalize. I was one step away from getting my card. That’s what I thought anyway.

While Home Trust does allow transfers from over 100 different financial institutions, the KOHO account I used wasn’t one of them. There is a link that says “Can’t find your institution?” but that link is broken. So there was an additional delay while I transferred money.

Once the transfer was complete, I went back to it. Home Trust uses a company called Flinks to process their banking transactions. After agreeing to that, the bank transfer began.

But it timed out mid-process. Then the application itself timed out.

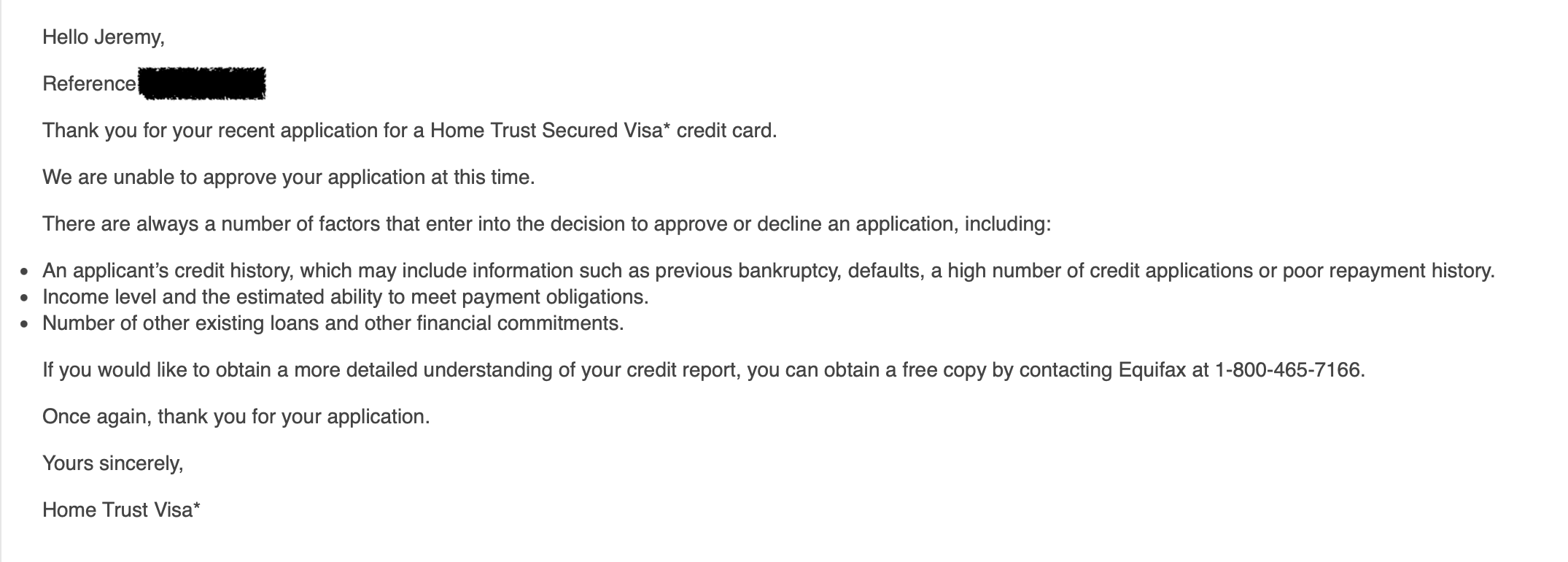

Several months of back and forth, and I still had $500 that Home Trust refused to touch. As of this writing, my customer service file is still open.

This doesn’t appear to be an isolated incident. On Reddit, when asked for opinions on Home Trust one user replied, “They are legit, but I cannot recommend them: their online banking is from [the] 1990s.”

They currently have a 1.5 star rating on TrustPilot based on 102 reviews. Many of which describe similar issues. Their latest Better Business Bureau complaint comes from an irate software engineer claiming their software update causes an infinite loop that makes logging in impossible.

I do not have a card. I have stopped expecting one.

People who need secured cards don’t have the capacity to endure a three-month bureaucratic ordeal. They’re in a rebuild. They’re waiting on a lease application, a job that runs a credit check, an unpaid bill they need to put somewhere.

Home Trust is a Kafkaesque nightmare. The best rate, the highest barrier, the most broken process, and the people most capable of navigating it are the people least dependent on the card.

Verdict: The Home Trust card is Schrödinger's financial product: it’s got good terms but may not actually exist.

Credit Score Impact

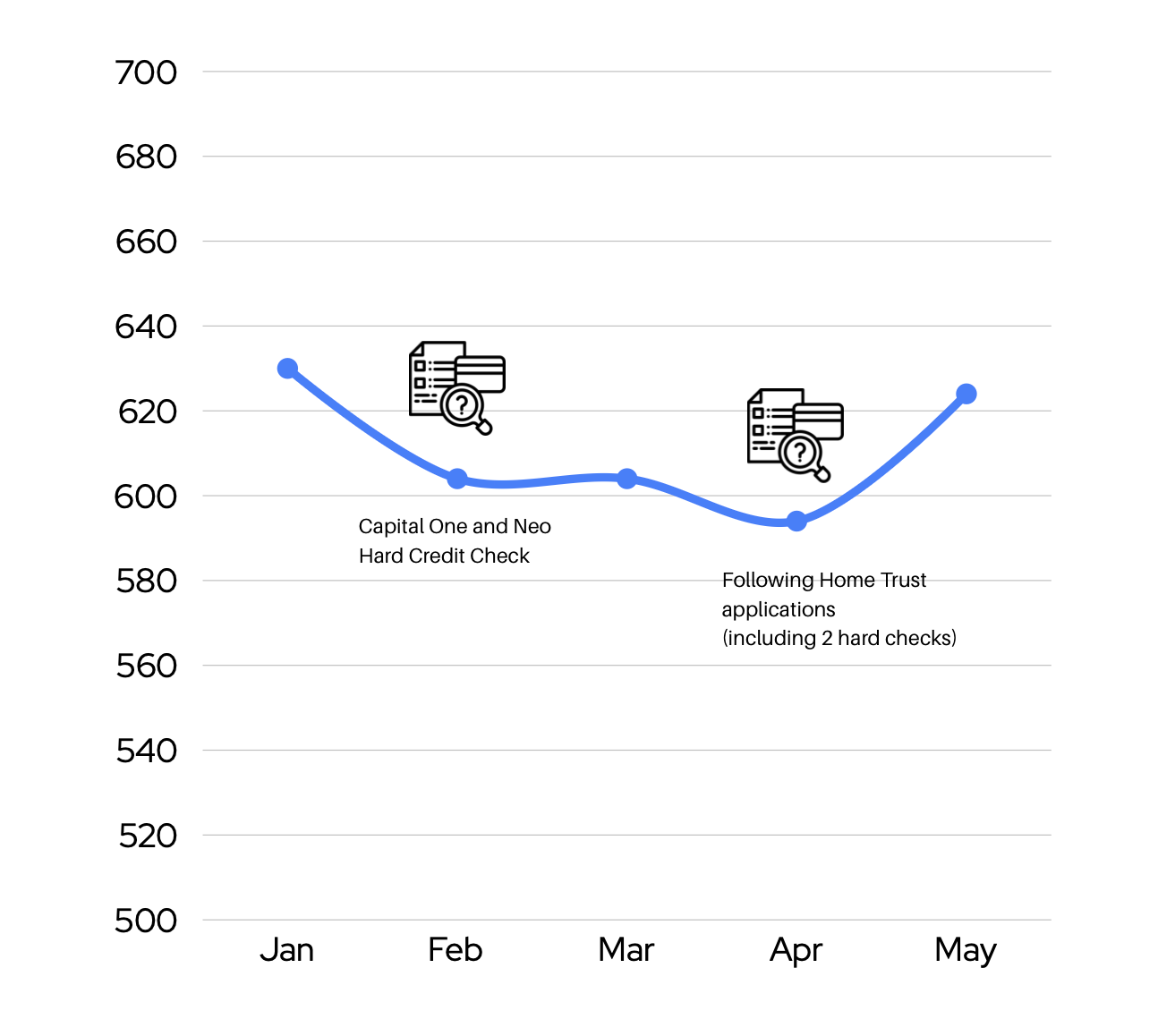

I started in January at 630. The applications pulled it down. That's normal, expected, part of the process. By April I was at 594. It’s started to rise again now that I’m no longer applying for the Home Trust card every week. My most recent score was 624.

While the applications did lower my score temporarily, the subsequent reports showed movement in a decidedly upward direction. I have two secured credit cards. They work. My score is moving, and that’s all that matters.

Bottom Line

Capital One if you need it today.

Neo if money is tight or you care about cashback.

Home Trust if you have $500, patience, and nothing better to do. If you get one, call me. I want to know how you did it.

Update

After months of attempts that went nowhere and $500 that I ended up spending on rent, it turns out I was not approved for the HomeTrust card after all.

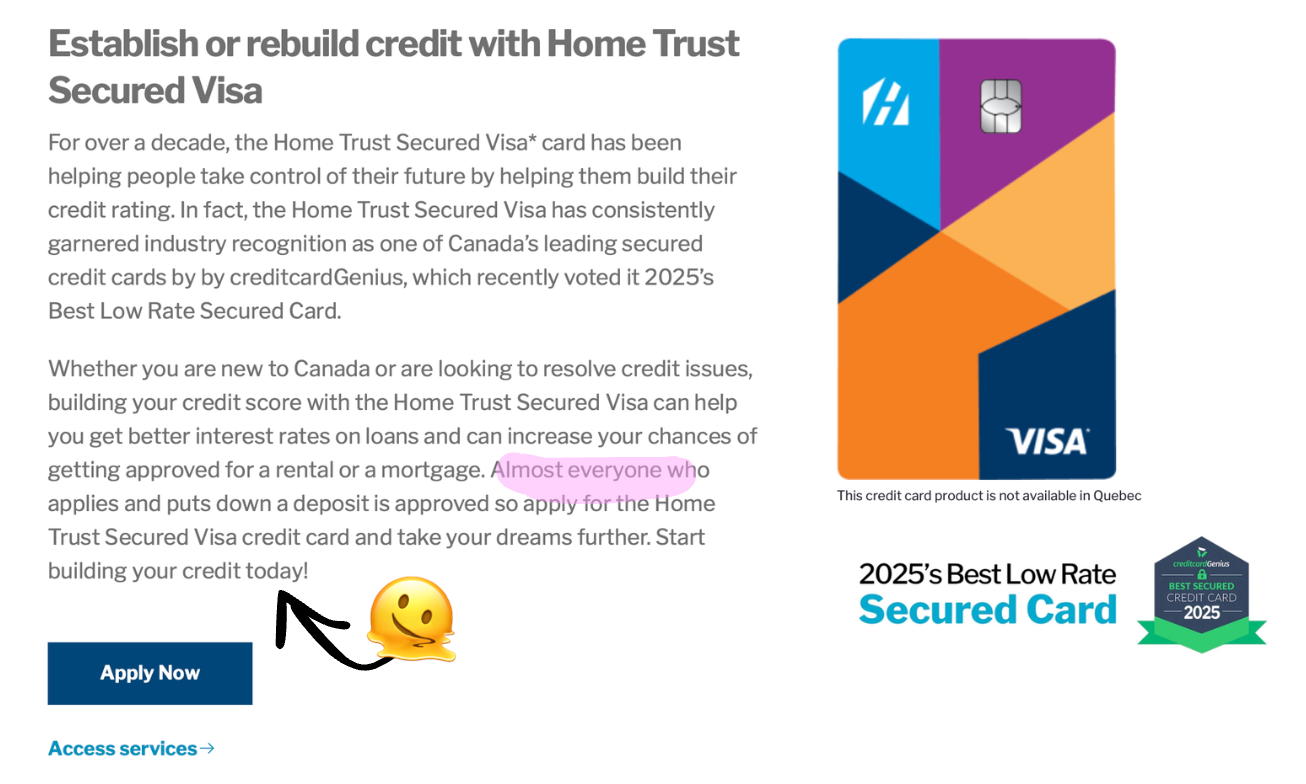

To be fair, they do specify that almost everyone is approved, which is a noted difference from the heavily-marketed “Guaranteed Approval” of Neo and Capital One.

At least I’m no longer getting a 403 error on the application page.

My verdict stands.