My boyfriend and I were applying for a new rental when I realized I had never properly checked my credit report in Canada. I always assumed it would be confusing and packed with upsells, so I kept delaying it.

But this time, I decided to turn it into a small experiment. I pulled both of our free credit reports from Equifax and TransUnion. I expected the reports to be boring and identical. Surprisingly, some information showed up on one report but not the other. One report even listed an address I have never lived at! Before spiraling, I called two credit experts to understand what I was seeing. Here’s what happened when I compared both reports side by side.

Did you know that no matter what your credit score is, you can get instantly approved for Secured Neo Mastercard? Plus, sign up now via the button below and get a $60 welcome bonus.

* Limited-time offer. Only valid for new Neo customers who open their first eligible Neo credit product and make a purchase within 90 days. Limit of one offer per customer. Offer is subject to the Neo Rewards Policy and may be amended or cancelled at any time without notice.

Getting our free Equifax credit reports

Finding the free Equifax report was easier than I expected. The first few links pushed paid products, but the free option was still there if you scrolled past them. Before signing up, I double-checked with an official guide that I was using the correct report links.

The signup process was fairly simple. I entered my name, address, and contact details, went through account verification, and created a login.

The first things I checked on my report

Before getting lost in numbers, I checked the basics. My name, address, and whether the accounts listed were actually mine. That advice came up in both expert conversations I had. One of them was Himank Bhatia, an Education Program Lead at Credit Canada. He told me: “Before looking at any numbers, verify the personal information on the first page. If that data is wrong, the rest of the report is basically meaningless.” Vasu, the other expert I spoke to, said the same thing more bluntly: “If the name or address is wrong, you have to contact the credit bureau. That’s the first red flag.”

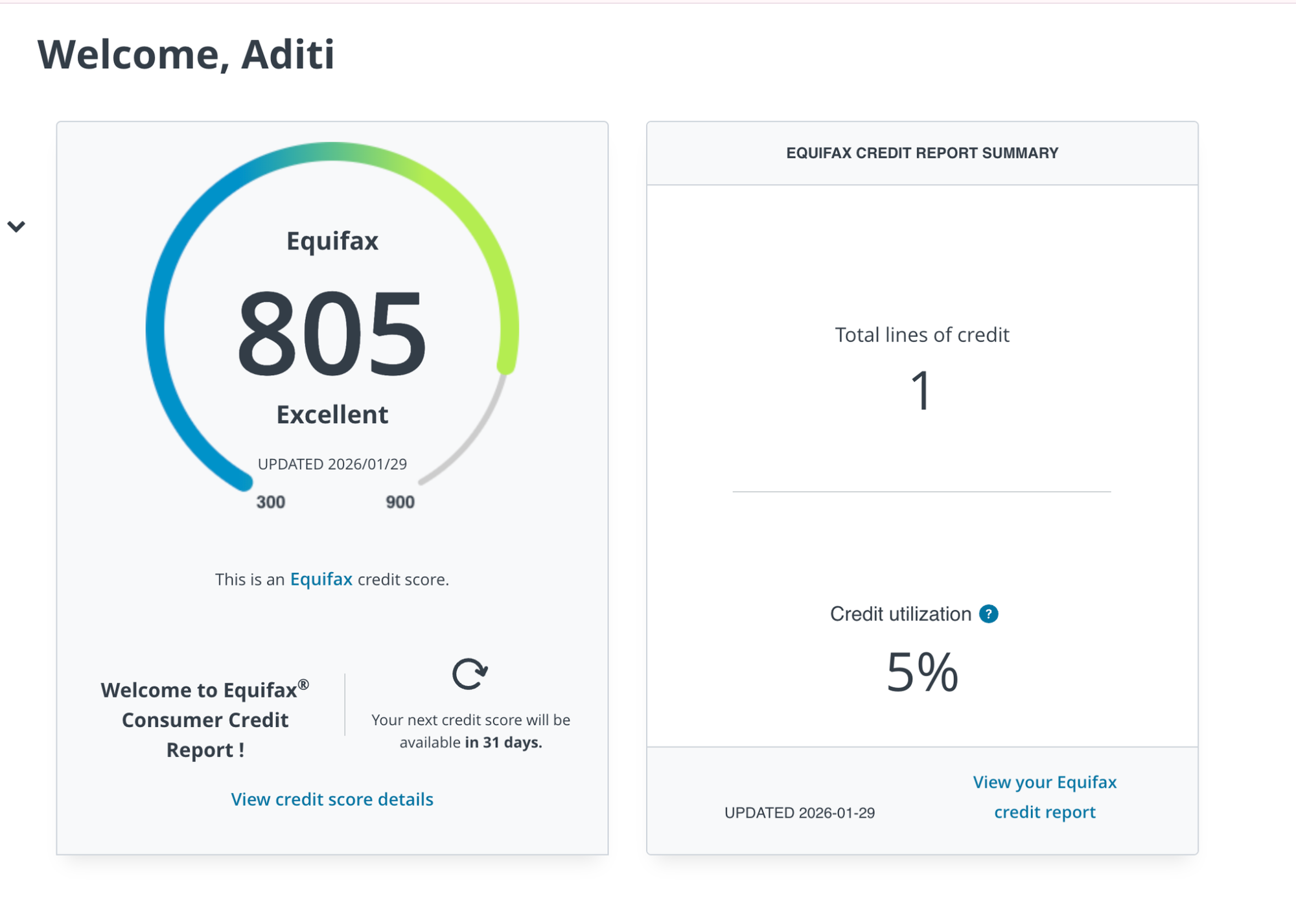

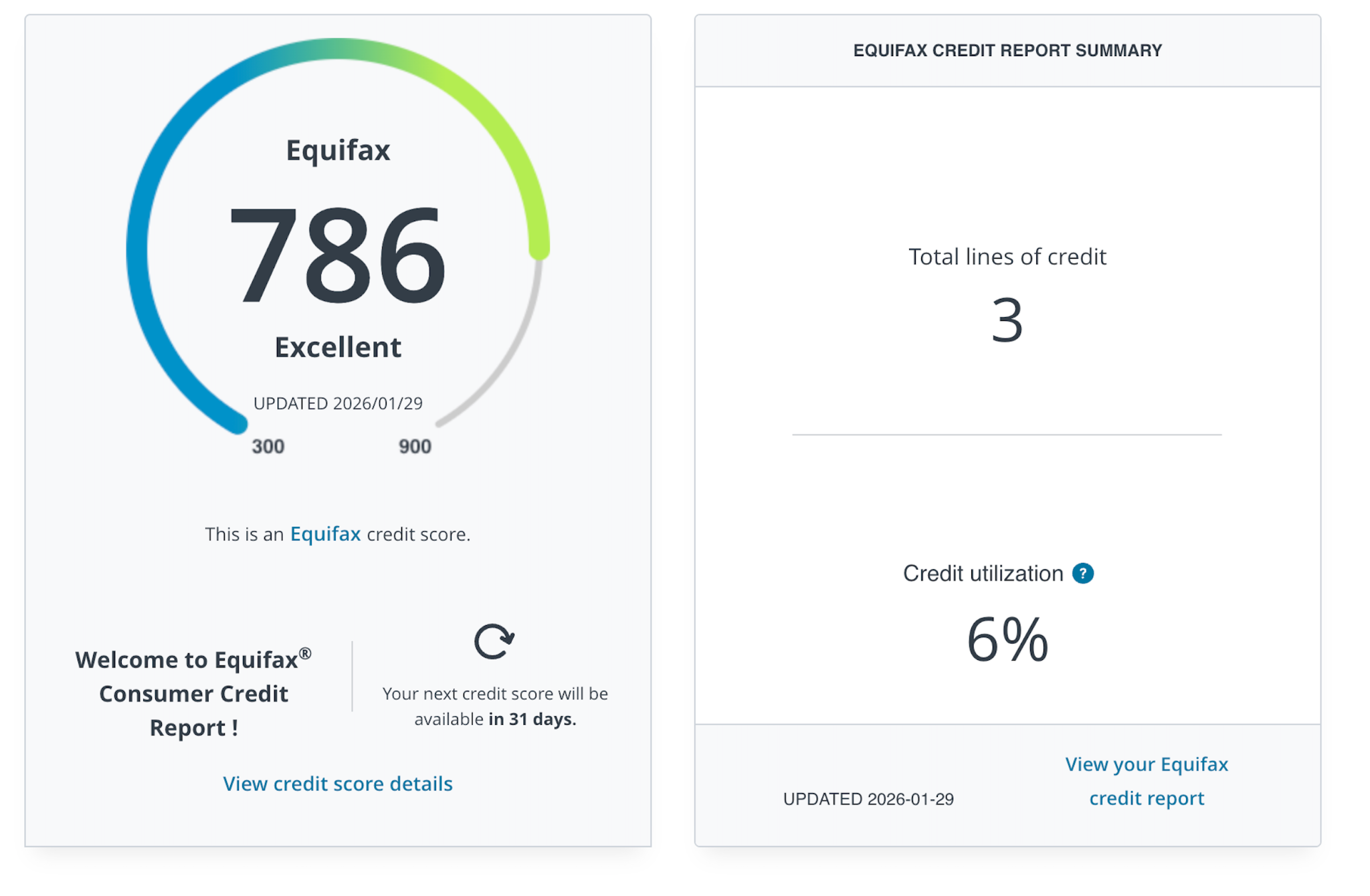

Only after that did I look at my credit score. It was 805, and the “excellent” label instantly brightened the overachieving kid in me. My boyfriend’s score was 786. Still strong, but slightly lower than mine. That comparison was interesting because he has been in Canada longer than I have, with almost identical credit utilization. It reinforced something both experts emphasized: credit scores reflect patterns and not isolated moments.

The Equifax lines that made me stop and reread

When I opened my report, a few lines immediately threw me off. One said, “You have no positives affecting your credit score.” Another said, “You currently have no employment history on your credit file.” That was confusing, especially since I do have a full-time job and pay my bills on time.

Himank explained that employment information is often missing because employers do not report directly to credit bureaus. The only time Equifax usually knows where you work is if you listed your employer on a credit application in the past. The “no positives” line also does not mean you are doing something wrong. It often shows up when a credit file is thin or still fairly new. As long as payments are on time, this language is usually nothing to worry about.

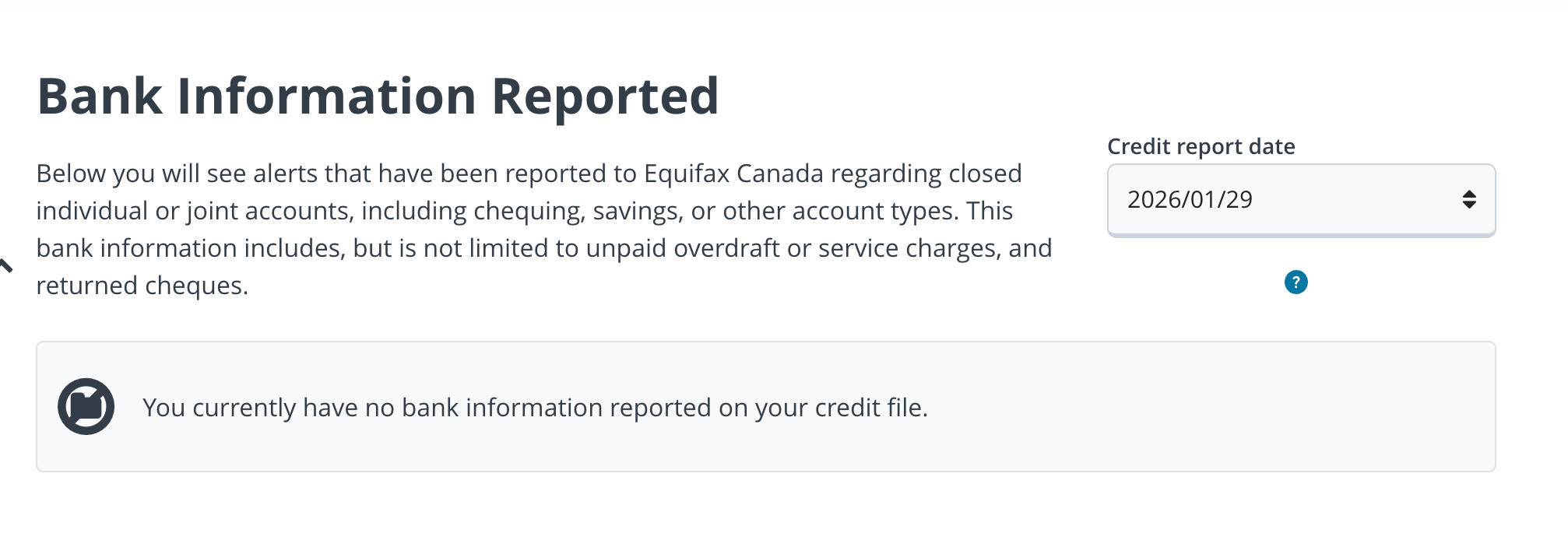

What didn’t show up on my Equifax report

I noticed that two bank accounts I had closed were not listed at all. I had recently closed a chequing account and a savings account, but neither appeared on my report. Even for my boyfriend, his old Scotiabank savings account didn’t show up. At first, I assumed this was a reporting error.

But Himank, the Education Program Lead at Credit Canada, explained that this is usually something you can ignore. “Credit reports are mainly for loans and credit cards. Regular chequing and savings accounts usually don’t show up unless there was overdraft credit or a negative balance sent to collections.”

He also pointed out that missing information is not always a bad thing. Unless an account was a long-standing credit line that helped build years of positive history, it usually isn’t worth the paperwork to add it back.

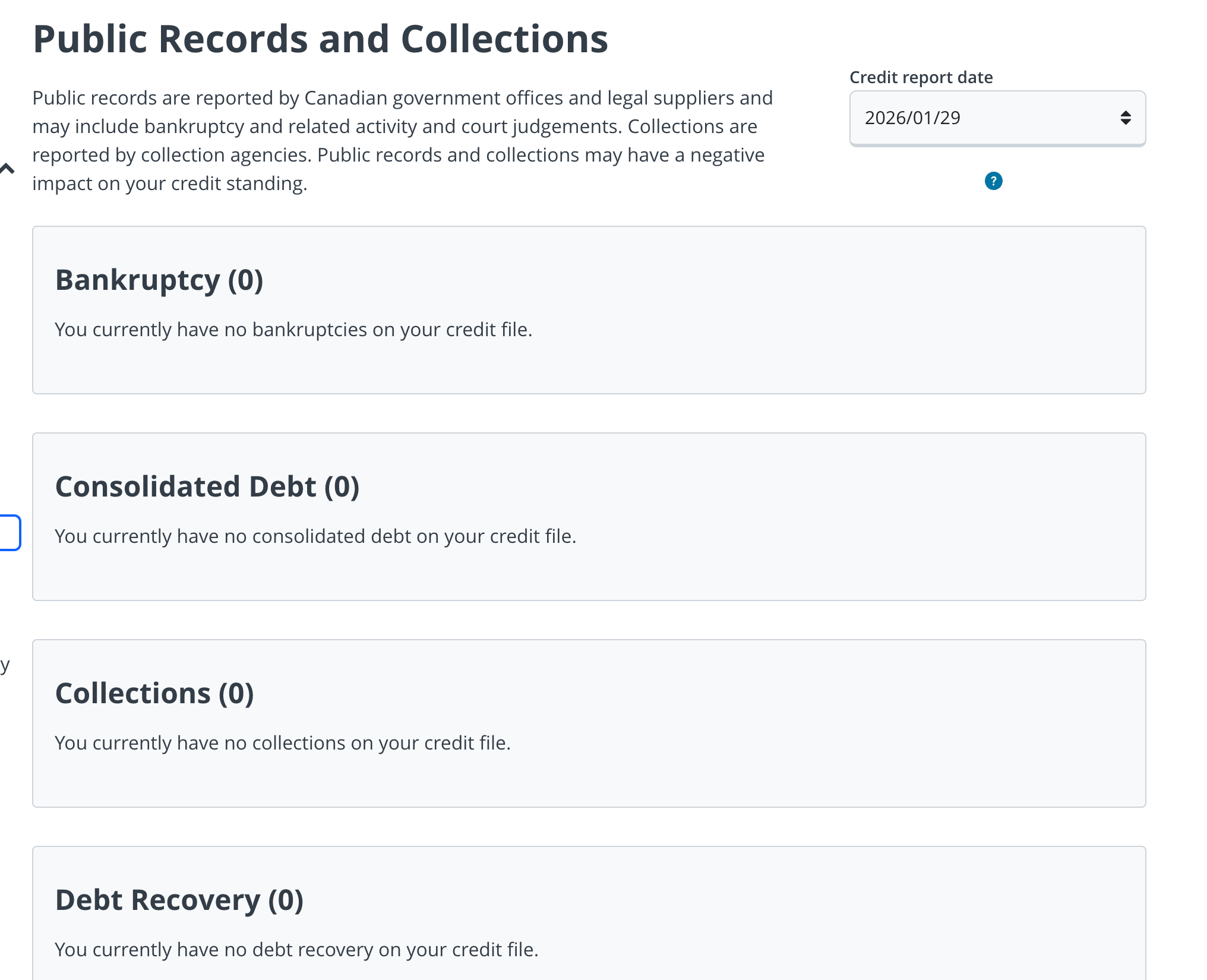

The section I was secretly nervous to open

There was one section I clicked on with a bit more hesitation: Public Records. This is where things like bankruptcies or court judgments show up. In credit report language, these are often called derogatory items. They’re serious negative marks that can make it much harder to get approved for credit, rent an apartment, or qualify for a mortgage.

Mine was empty; not a shock but still a relief.

When I asked Himank about this, he added a word of caution. In Canada, most negative items stay on your credit report for about six years from the date of the first missed payment. Even if you eventually pay it, the record does not disappear overnight. And if you have multiple bankruptcies, the second one can stay on your TransUnion report for up to 14 years.

He also added that the damage is not just about how long it stays. It’s about how recent it is. A missed payment from five years ago hurts far less than one from last month.

Trying to get my free TransUnion credit report

Getting the free TransUnion report took more effort than Equifax. The site strongly pushes paid products, and I couldn’t find the free version through normal browsing. I eventually found the correct link on Reddit.

The TransUnion issues I couldn’t ignore

The signup process raised my first red flag. I had to verify personal information to confirm my identity. The problem was one of the multiple-choice questions where I had to confirm my previous address. None of the options was correct, so I picked a random answer just to move forward. Somehow, my account still got verified. The whole thing didn’t sit right with me.

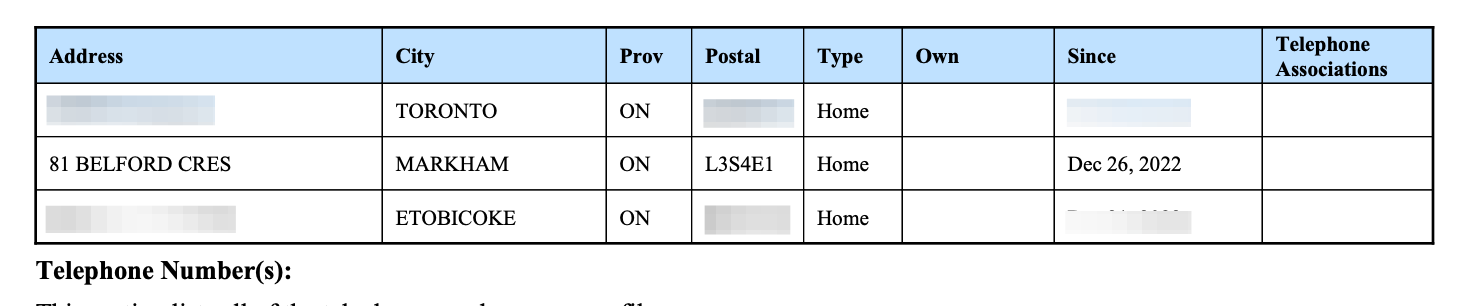

After getting access to my report, I noticed something more serious. TransUnion had added an address I have never lived at. I suddenly remembered the experts’ advice that a random address is not just a typo. It’s a red flag and should be disputed as soon as possible.

A wrong address can mean your file was mixed with someone else’s or that your information was entered incorrectly by a lender. I ended up raising a dispute with TransUnion for this reason.

What showed up on our TransUnion reports

One notable limitation was that TransUnion did not include a credit score in the free report. To see it, I would have had to upgrade to a paid plan. However, you can use Credit Karma to see your TransUnion credit score. I didn’t dwell on it much because the credit experts told me the score is just a shortcut. It’s the credit report itself that lenders actually read.

Aside from the address issue, the rest of my report looked internally consistent. My account opening dates, last payment dates, and last reported dates all lined up.

Compared to my Equifax report, TransUnion showed more hard credit checks. These were tied to things I clearly remembered, like opening my account and requesting a credit limit increase.

How soft checks showed up on both reports

I noticed a weird pattern while comparing both reports. My TransUnion report showed soft checks from Wealthsimple, while my Equifax report showed soft checks from Borrowell. The opposite checks were missing in each report. When I looked at my boyfriend’s reports, some soft checks appeared on one bureau but not the other.

At first, it looked inconsistent. But soft checks don’t impact your score. They often happen when you check your own credit through apps, when a bank reviews your account internally, or a credit score app pulls checks. They’re visible to you, but not to lenders evaluating a new application.

“Soft checks are usually no concern at all,” Vasu, the other expert, told me. “People fear them, but they don’t affect your score.”

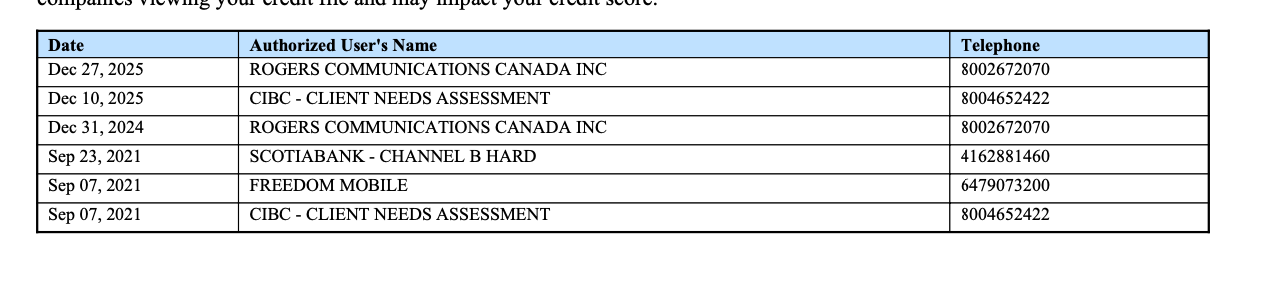

What I learned from comparing hard inquiries

On my reports, TransUnion showed hard inquiries tied to things I recognized, like opening my account and requesting a credit limit increase. Those same inquiries didn’t appear on my Equifax report. On my boyfriend’s reports, the gap was even wider. His TransUnion report listed six hard inquiries, including two from Rogers and one from when he opened his account. On his Equifax report, the only hard inquiry was from Virgin Mobile.

This time, the mismatch made me pause because I know hard inquiries are visible to lenders and they impact your score. But Himank, who's an Education Program Lead at Credit Canada, reassured me that differences alone aren’t a problem. You’ll often see more hard inquiries on one report simply because that lender chose to pull from that bureau only. He also clarified the difference between normal mismatch and a real problem: “If you see a hard inquiry or account from a company you’ve never dealt with, that’s a red flag and should be disputed.”

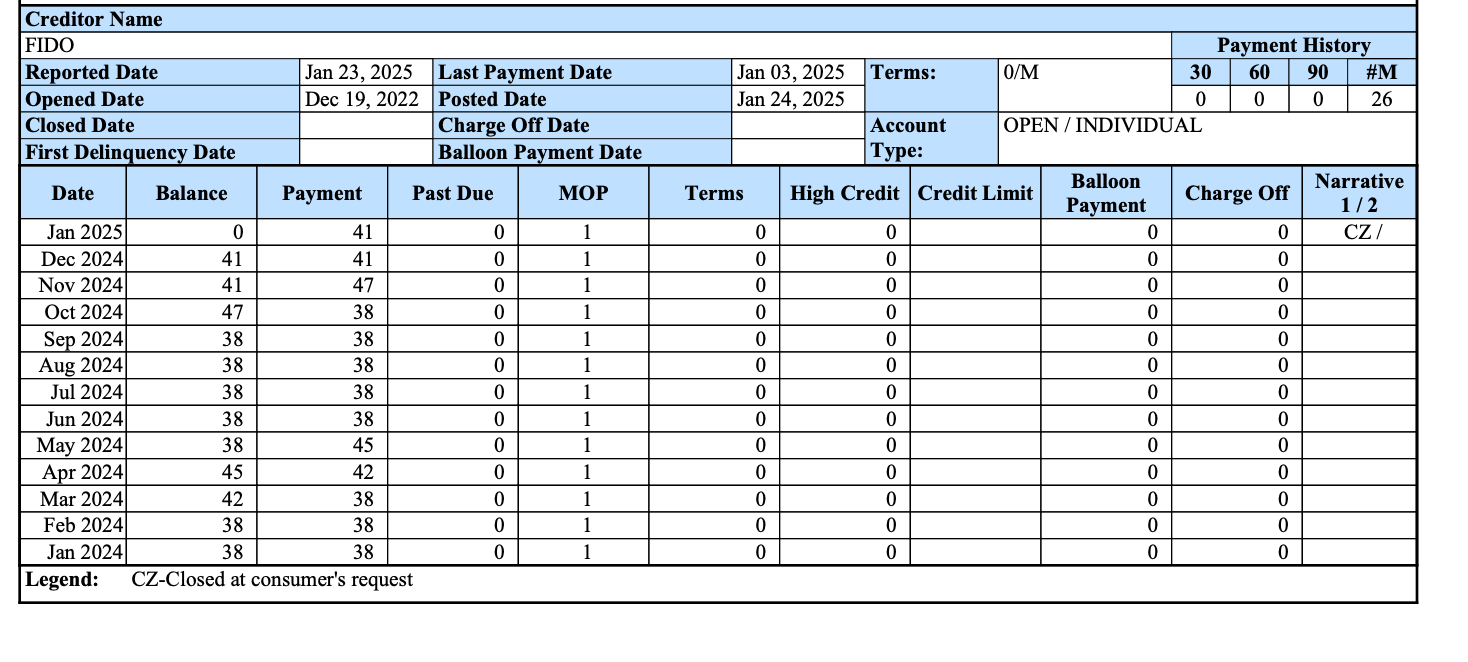

Phone bills were the most chaotic part of our reports

My old Fido connection showed up under “OPEN / INDIVIDUAL” debt on TransUnion, but it did not appear at all on Equifax. Seeing it listed on one report and missing on the other immediately raised questions.

On my boyfriend’s reports, it was much more confusing-

- Virgin Mobile: His old Virgin account showed up as “OPEN” debt on both Equifax and TransUnion. However, only Equifax listed a hard inquiry from Virgin. That same inquiry did not appear on TransUnion.

- Rogers: His current Rogers account did not show up as an open debt on either report. But TransUnion listed two hard inquiries from Rogers, which were completely missing in Equifax.

It looked messy, but both experts told me this kind of uneven reporting is common with phone providers. Payment updates, inquiries, and account details don’t always appear in the same way across reports. Himank explained it simply: a missing “good” phone account usually isn’t worth disputing because phone bills are just bonus credit data. The only time they deserve attention is when a phone account or inquiry looks unfamiliar or incorrect.

Phone bills turned out to be more like background noise.

When I decided to file a dispute with TransUnion

Most of the mismatches I saw didn’t need fixing. But the random address on my TransUnion report was more serious than a missing phone bill or an uneven inquiry. So I filed a dispute directly through TransUnion’s online portal. The form was simple. I selected the incorrect address, marked it as inaccurate, and submitted the request. Within five days, I received an email confirming that the address had been removed.

Not every inconsistency is a crisis, but when it comes to identity details, it’s better to fix it than to hope it doesn’t matter.

The credit report advice that actually stuck with me

After comparing four reports and talking to two experts, I realized most of my stress came from not knowing what to focus on. The first thing to check is your personal information. Your name, date of birth, and addresses need to be correct. Next, look at your active accounts. Are they actually yours and are the balances accurate? If you see an account you never opened, that’s when you act.

You can usually skim old employment history, soft checks, and closed accounts that were paid properly.

One thing Himank emphasized that really stuck with me is that the report matters more than the score. Lenders look at the story underneath. Do you pay on time? Do you carry reasonable balances? Are the accounts actually yours? And when it comes to improving your credit, the advice was almost boring in its simplicity. Pay on time and keep your balances low. That’s it. Vasu put it bluntly: “Don’t spend money you can’t pay back.”