It’s been a few years since I signed up for KOHO, Neo, Wealthsimple, and EQ Bank. But I do remember the applications were fast and straightforward. KOHO, Neo, and Wealthsimple all gave me instant digital access to a virtual card while I waited for the physical version to arrive. EQ Bank and BMO do not provide virtual cards, which immediately puts them a step behind their competition.

To see how these five cards stack up in real life, I put each one to the test. I loaded them with $25 each and made at least one transaction per card. Here’s what I’ll keep and what I’ll cut up.

Neo Money Card

I started with the Neo Money Card and used it to stock up on my kid’s school snacks, since those were groceries I was already planning to buy. I’ve had the Neo Money Card for a few years and still use it occasionally for bonus cashback offers through their partner network.

I loaded $25 via eTransfer from my Tangerine account at 3:27 p.m. The funds arrived four minutes later, at 3:31 p.m. Not as quick as KOHO, but fast enough in my opinion.

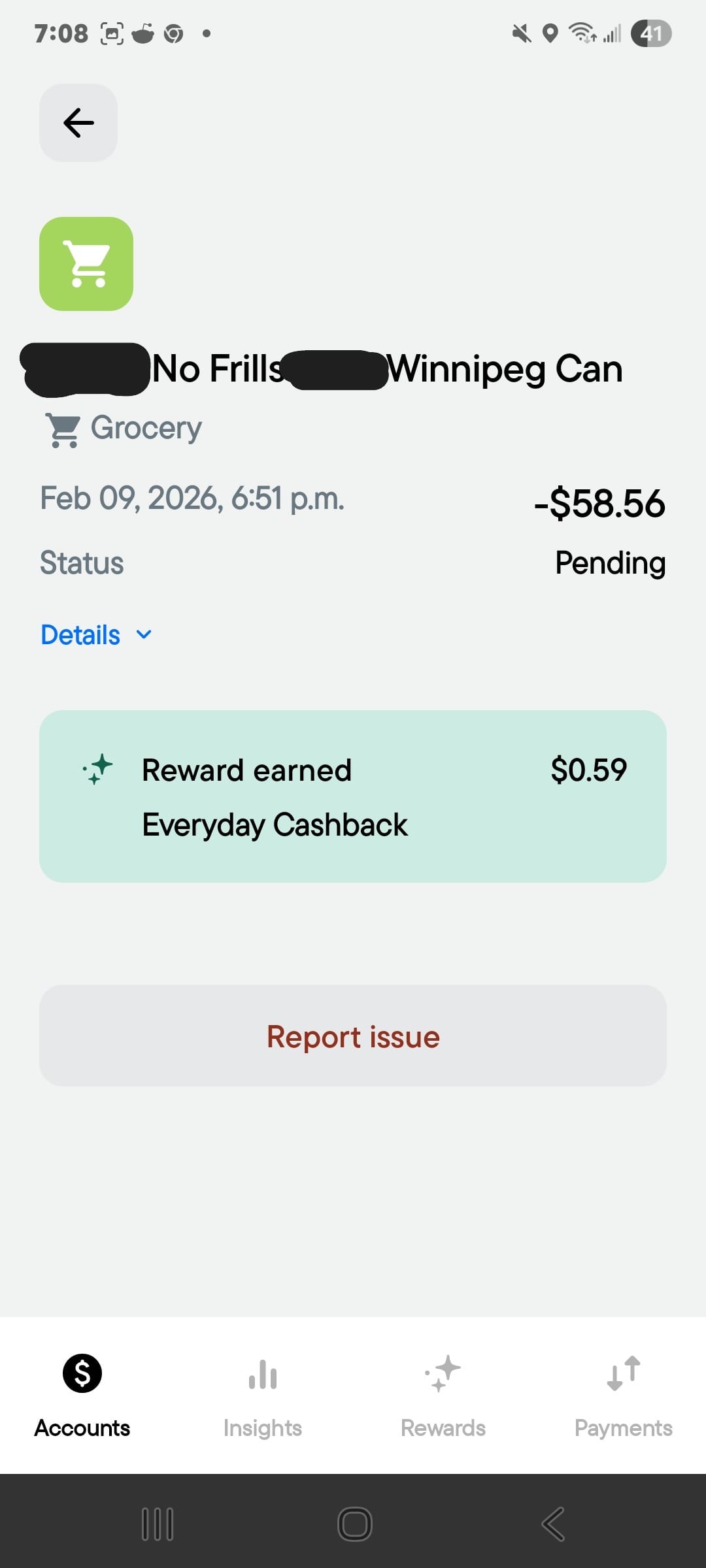

Next, I headed to No Frills with my Neo Money Card in tow. I spent $58.56 on groceries and earned 1% cashback, which was $0.59. My cashback was available very quickly, either that same day or the next, I can’t remember. I was able to cash it out to my Neo Money account without any issues.

I prefer Neo’s app interface over KOHO because it's more intuitive and better organized, in my opinion. The cashback marketing info matched what actually happened. There was no confusion about whether or not I would earn cashback on my grocery store transaction.

KOHO Prepaid Mastercard

Then I tested the KOHO Prepaid Mastercard. I’m already a customer and have always had a good experience with them. While I haven’t used the card in the last few years, I have kept it active.

I loaded the card with $25 through eTransfer from my Tangerine account at 2:22 p.m. The money showed up in less than a minute.

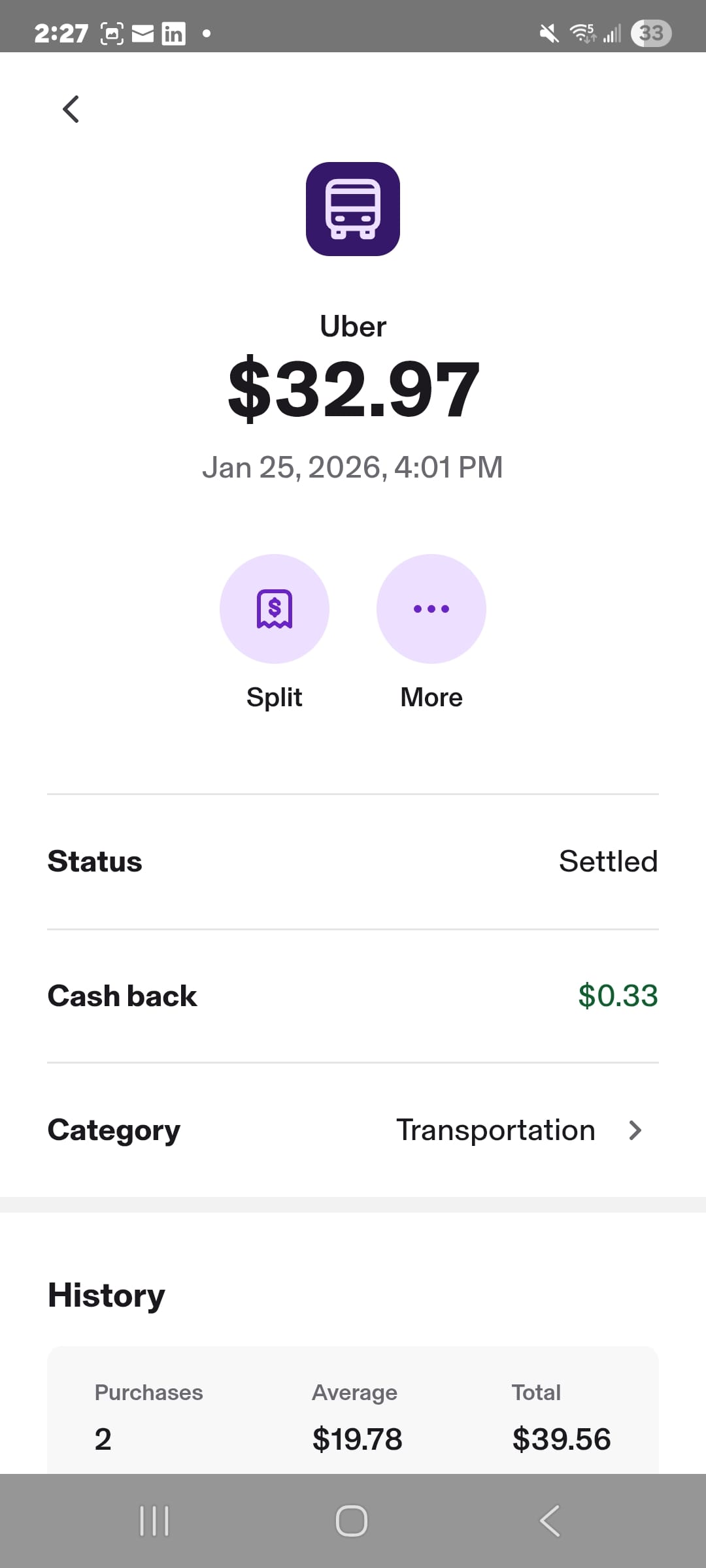

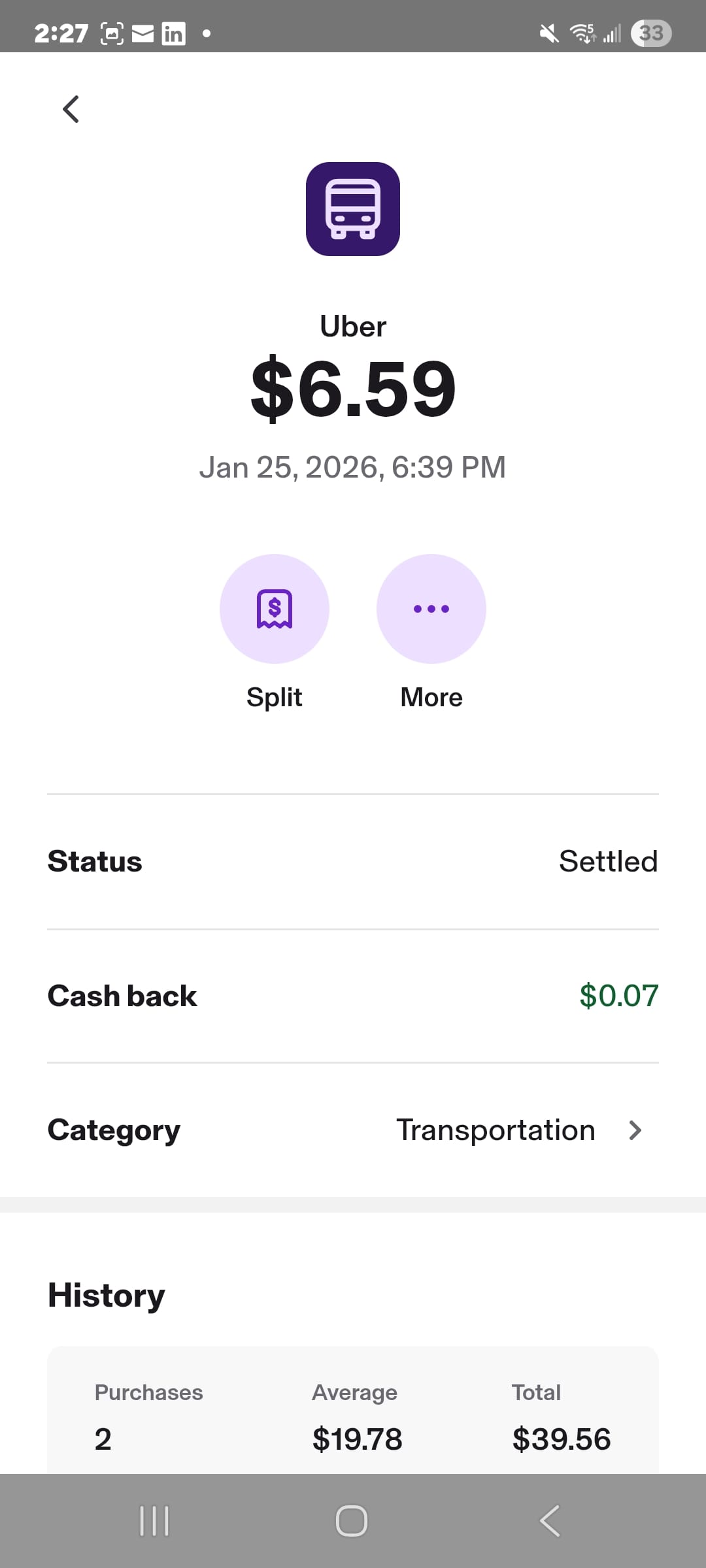

Next, I made a test purchase. My family was heading downtown to celebrate my nephew’s 18th birthday. It was -40, and parking downtown is always an absolute nightmare. Nobody wanted to deal with that nonsense in arctic temperatures, so we took an Uber.

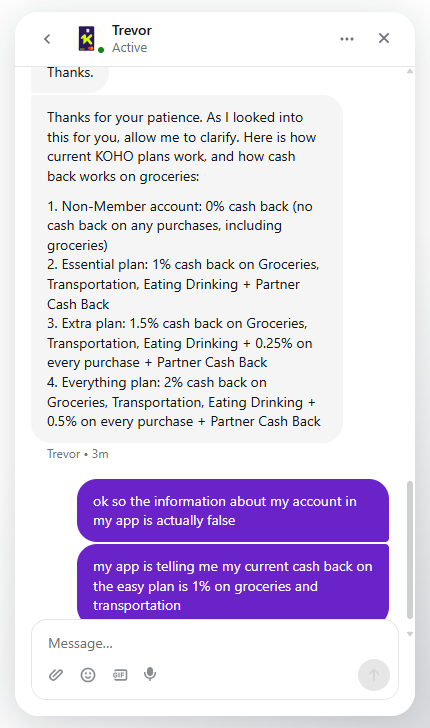

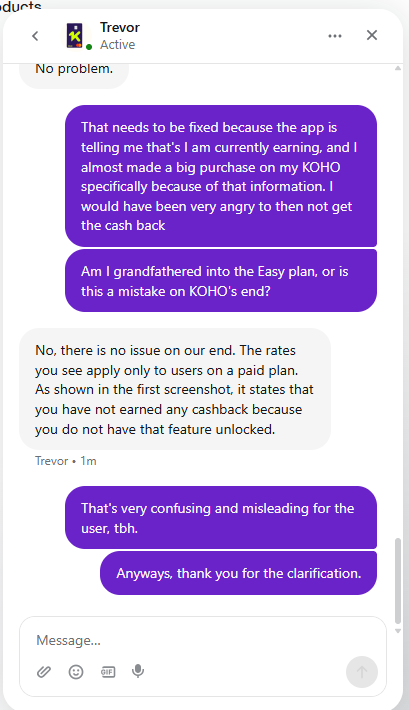

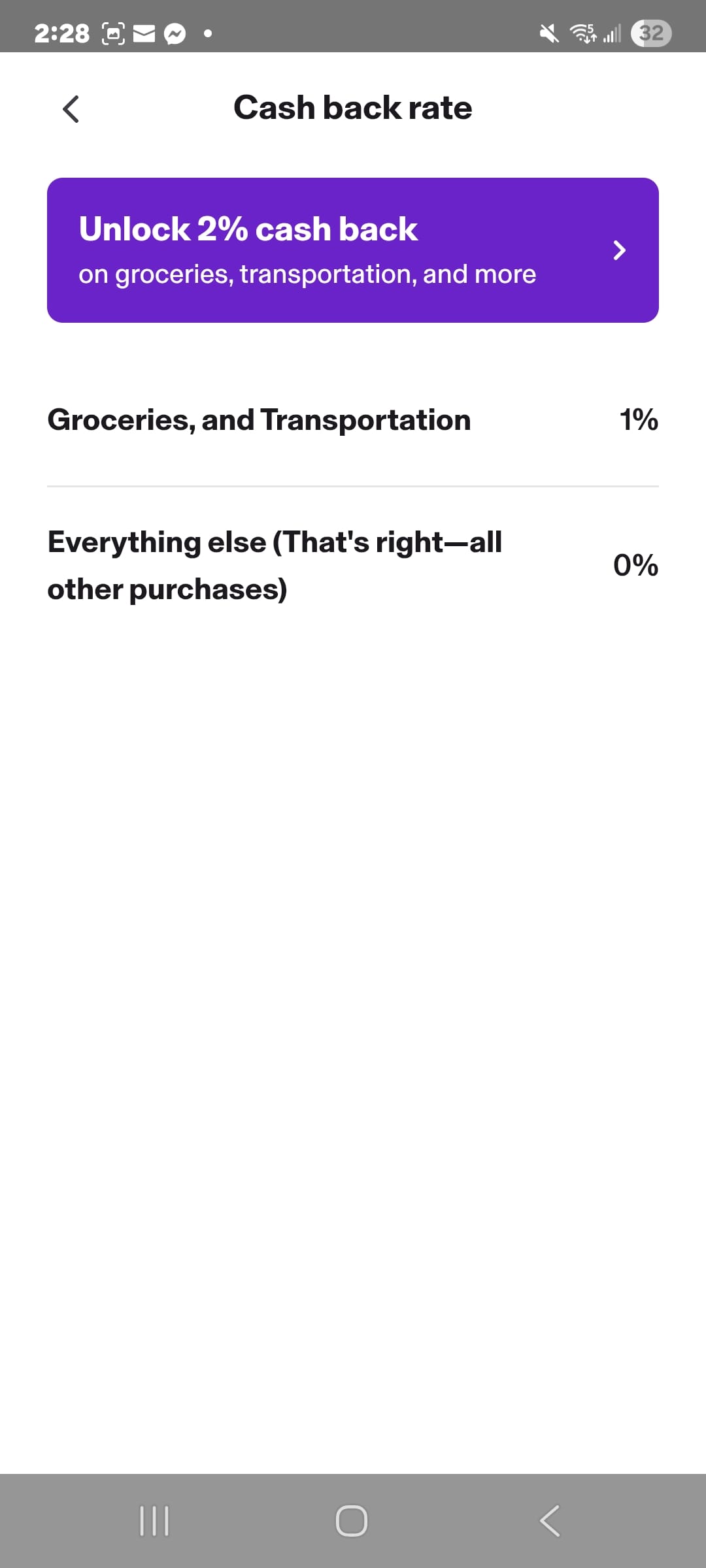

In the KOHO app, it said I’d earn 1% cashback on transportation, including rideshare. But KOHO changed its rewards structure since I last used the card. The messaging was both inconsistent and confusing. The app implied I would get the cashback, while the website suggested I wouldn’t unless I subscribed to a paid plan.

I contacted support and spoke to a live human agent. I sent screenshots from inside the app and asked if I would get cashback on Uber or not. The agent told me I would not, since I was on the free plan.

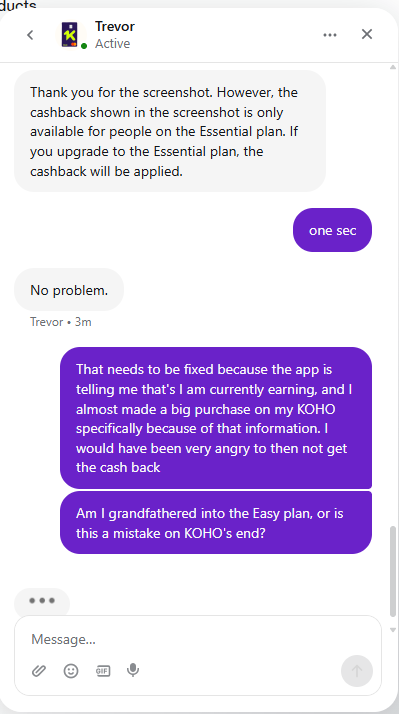

That irked me. I considered not using KOHO for the Uber. But it was already linked to my Uber account, and I needed to take the ride anyway, so I used it.

Later, I checked my KOHO app, and to my surprise, I DID earn cashback on the Uber ride, $0.40 to be exact. So the support rep actually gave me incorrect product info, which was frustrating.

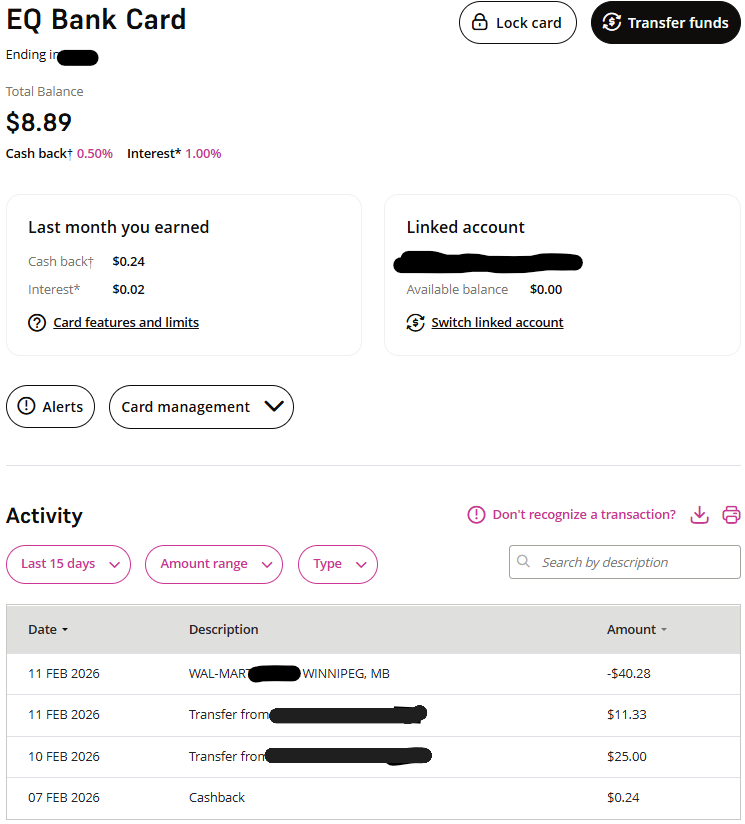

EQ Bank Card

Next up was the EQ Bank Card, which I already use for some business expenses like my LinkedIn Premium subscription. I like this card because I earn 0.5% cashback on all purchases without being restricted to specific spending categories. Unfortunately, loading this card is super annoying, and the app can be glitchy.

To load the card, I sent a $25 eTransfer from my Tangerine account at 2:39 p.m., and I got an email notification less than a minute later. But actually getting the money into my account took a lot longer.

It first started with the app experience. It was slow and glitchy, with fields not loading properly, and the screen kept freezing. I had to close all my apps and retry multiple times just to get through the eTransfer deposit steps.

The card also has an extra layer of friction because it uses a separate funding “bucket.” Even after the eTransfer was deposited into my account, the money didn’t show up on the card. I have to manually transfer funds onto it, and the card can only be linked to one EQ account.

Since I deposited money into my main EQ account rather than the account attached to the card, I had to move it from my main account to the linked account first. Then I had to transfer it again from the linked account onto the card. That’s a lot of steps for something other prepaid cards make pretty painless.

Then I used the EQ Bank Card at Walmart to buy a $40.28 birthday gift for a party my son was invited to. I should earn 0.5% cashback on that purchase, but EQ pays my earned cashback out monthly, which is slower and less satisfying compared to KOHO and Neo, where rewards are paid out almost instantly.

I consistently earn cashback on my LinkedIn Premium subscription, so I expect to receive $0.20 on the birthday gift purchase, and it should hit my account around the 7th of March.

I like earning cashback on all card purchases, even if the rate is a bit lower than competitors. In fact, EQ used to be my primary bank. But the app is clunky and glitches so often that I ended up switching to Tangerine for my day-to-day banking.

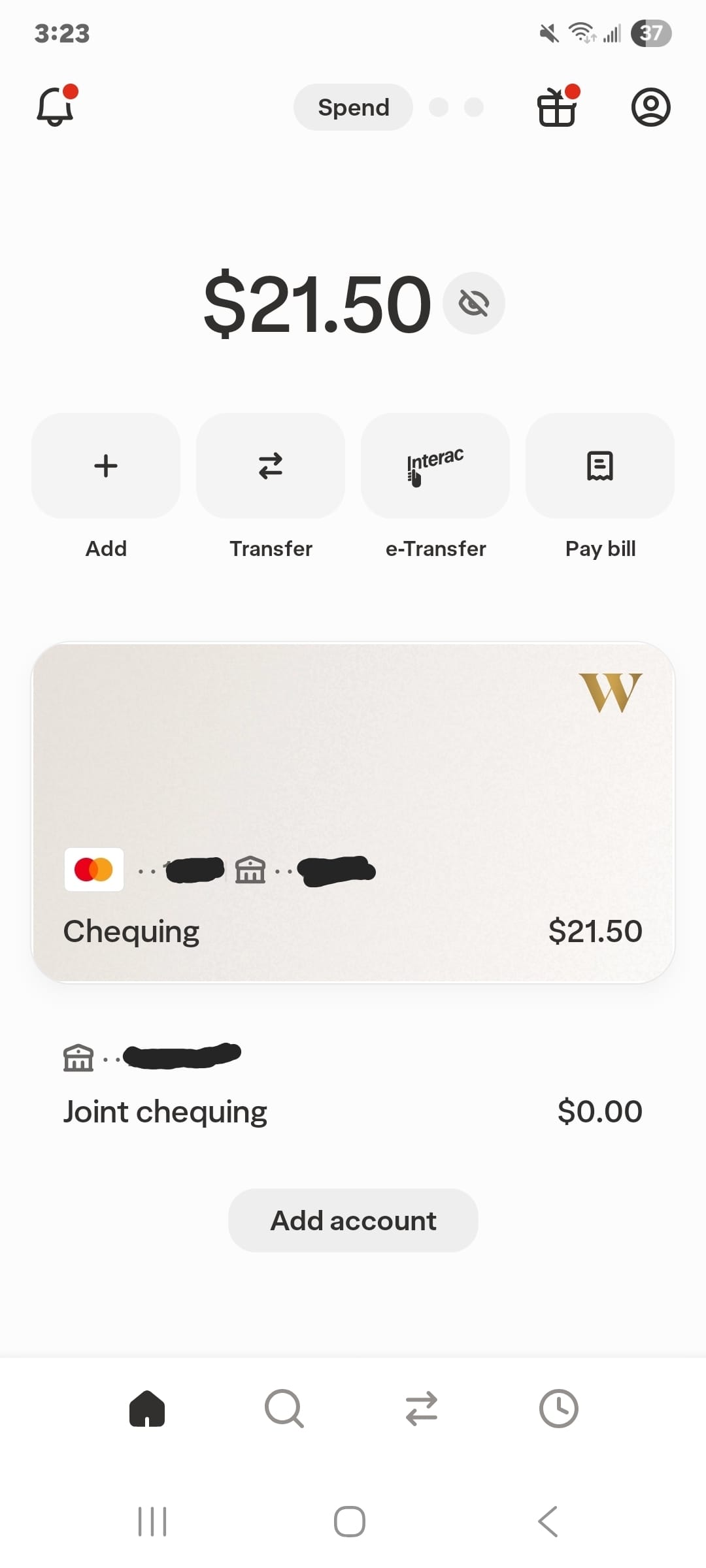

Wealthsimple Cash Card

There was a time I loved the Wealthsimple Cash Card and used it frequently, until they discontinued the cashback rewards. I was choked about that. But I kept the card for the simple fact that all my investments are with Wealthsimple, and they’re crypto-friendly. I have a client who pays me in crypto, so that makes it easier to access those funds when I cash to fiat.

I loaded this card with $55 from my Tangerine account by eTransfer, which arrived in less than a minute. I had originally planned to use this card for my son’s Walmart birthday gift, until I remembered I wouldn’t get any cashback. So I ended up using the EQ card instead, and sent some money from Wealthsimple to EQ via eTransfer.

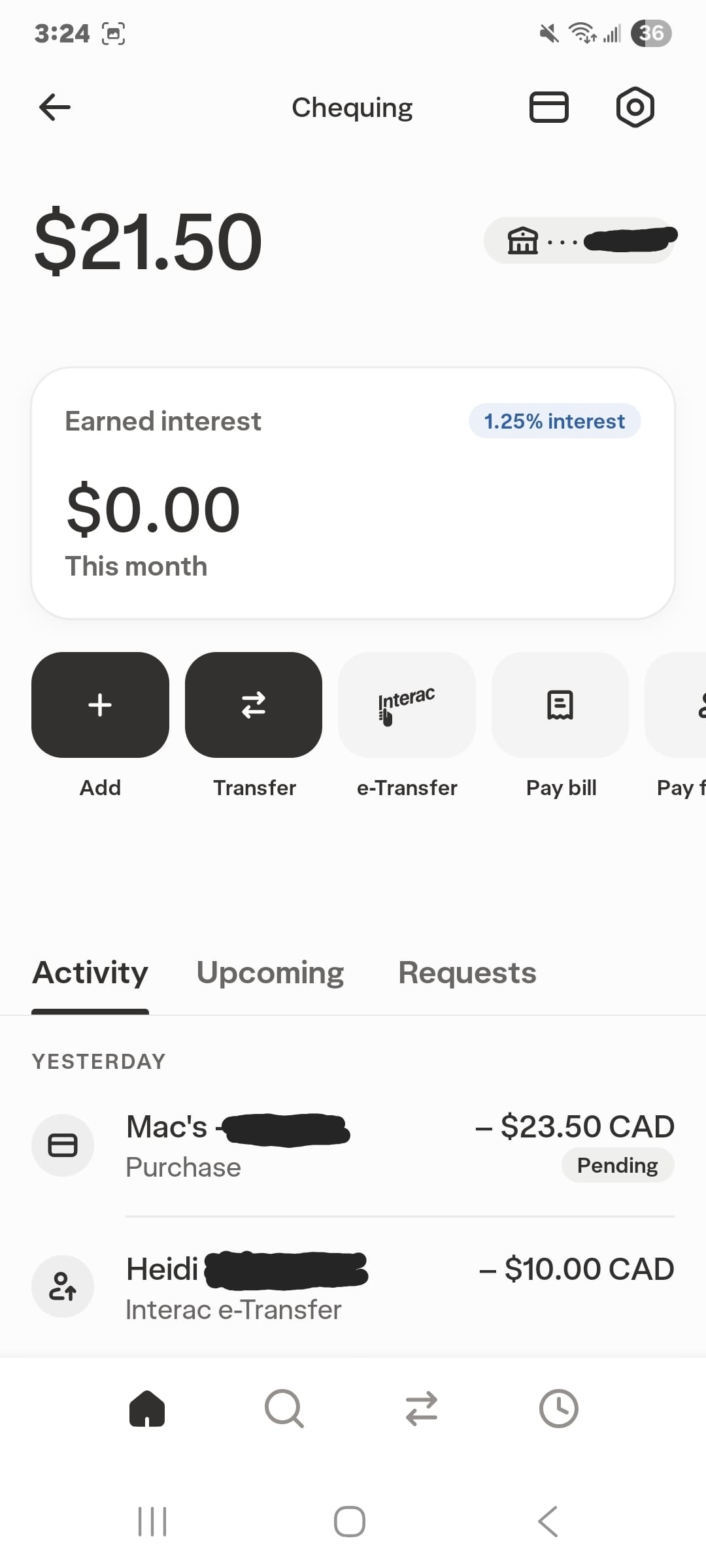

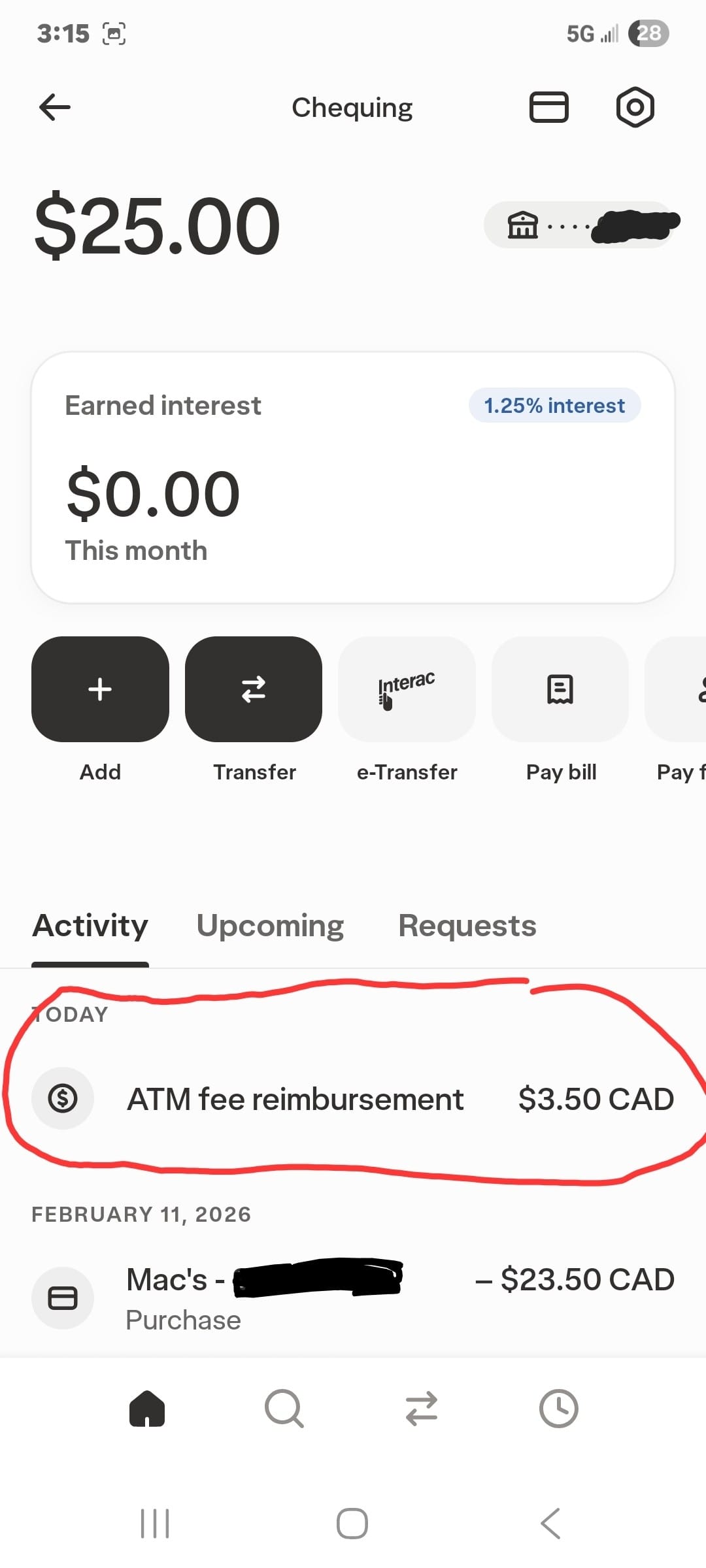

However, I was excited to discover that the Wealthsimple Cash Card will reimburse me for Canadian ATM withdrawals within 4 business days. So for the test transaction, I used it to withdraw $20 from the Circle K ATM near my house. The ATM charged me $3.50 for the withdrawal, and I was reimbursed two days later.

EQ also reimburses ATM fees, but they recently added new restrictions, and reimbursements take up to 10 business days. Wealthsimple is less restrictive and pays me back hella faster. That alone has suddenly made this card a lot more useful to me.

I was previously driving half an hour (both ways) to the nearest Scotiabank so I could use their ATMs to withdraw cash from my Tangerine account without fees. But now I can just eTransfer to Wealthsimple and walk next door to Circle K. I love that journey for me. But that’s the only time I’ll use this card.

BMO Prepaid Mastercard

This was the only prepaid card I didn’t already have. And after testing it, there’s only one word to describe it: Why. As in, why does the BMO Prepaid Mastercard even exist? Its functionality is archaic, and there isn’t a clear value proposition. It costs $9.99 per year and doesn’t even earn any rewards.

For a card with ‘travel’ in the title, I at least expected no foreign transaction fees. No dice. But hey, I get up to 20% off car rentals through select providers. Cool cool cool. How often do I need a rental car? Basically never.

The online application was quick, asked the standard questions all financial service providers ask, and it took about 5 minutes to complete. The site said I would receive an approval decision within 10 business days. But immediately after submitting the application, I received an approval email.

The email also said I would receive the card within 10 business days. Unlike competitors, BMO does not provide a virtual card. So you don’t even get instant digital access while you wait for the physical card.

Activation was unnecessarily complicated. The instructions told me to activate the card online, which did not work despite several attempts. I ended up calling in for help. The agent was genuinely pleasant and helpful, but a phone call shouldn’t be required to activate a prepaid card.

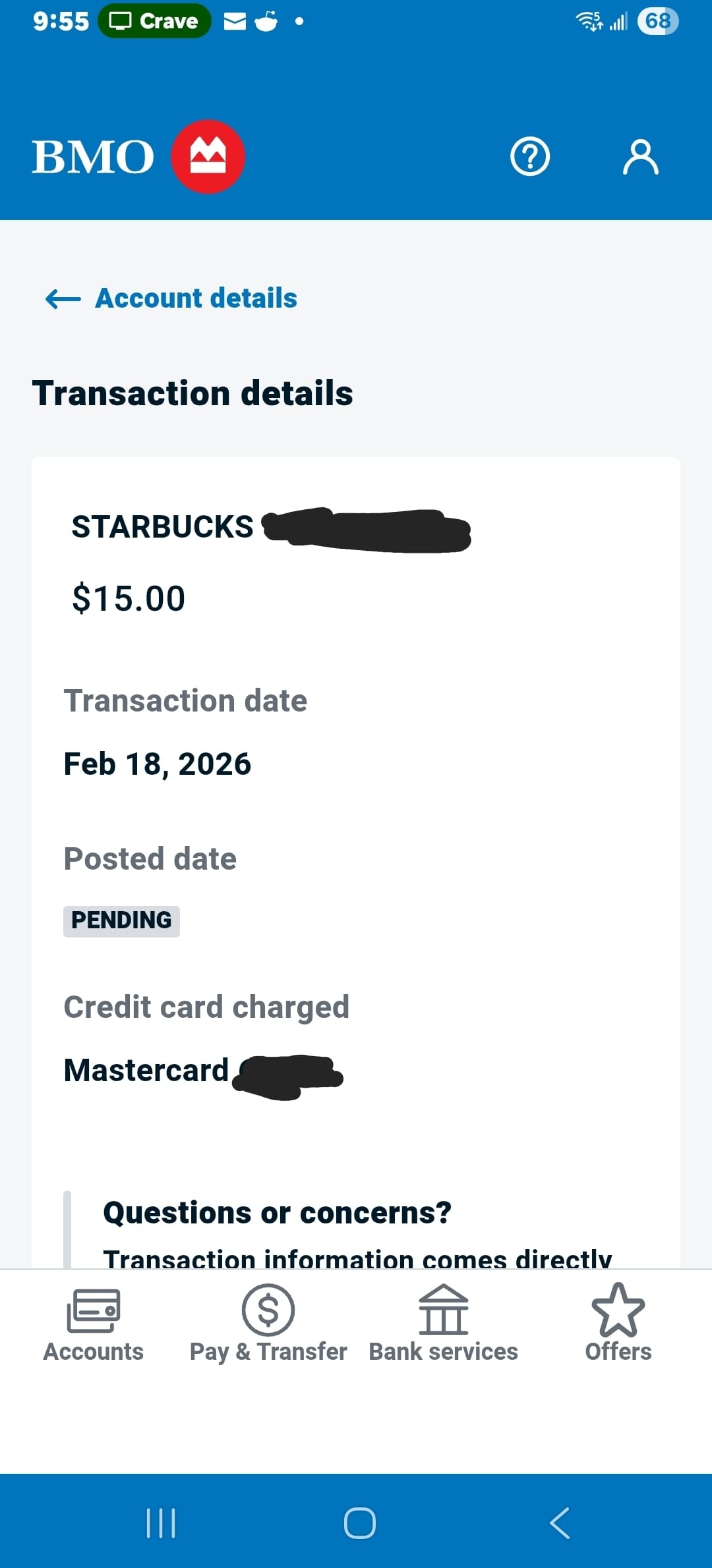

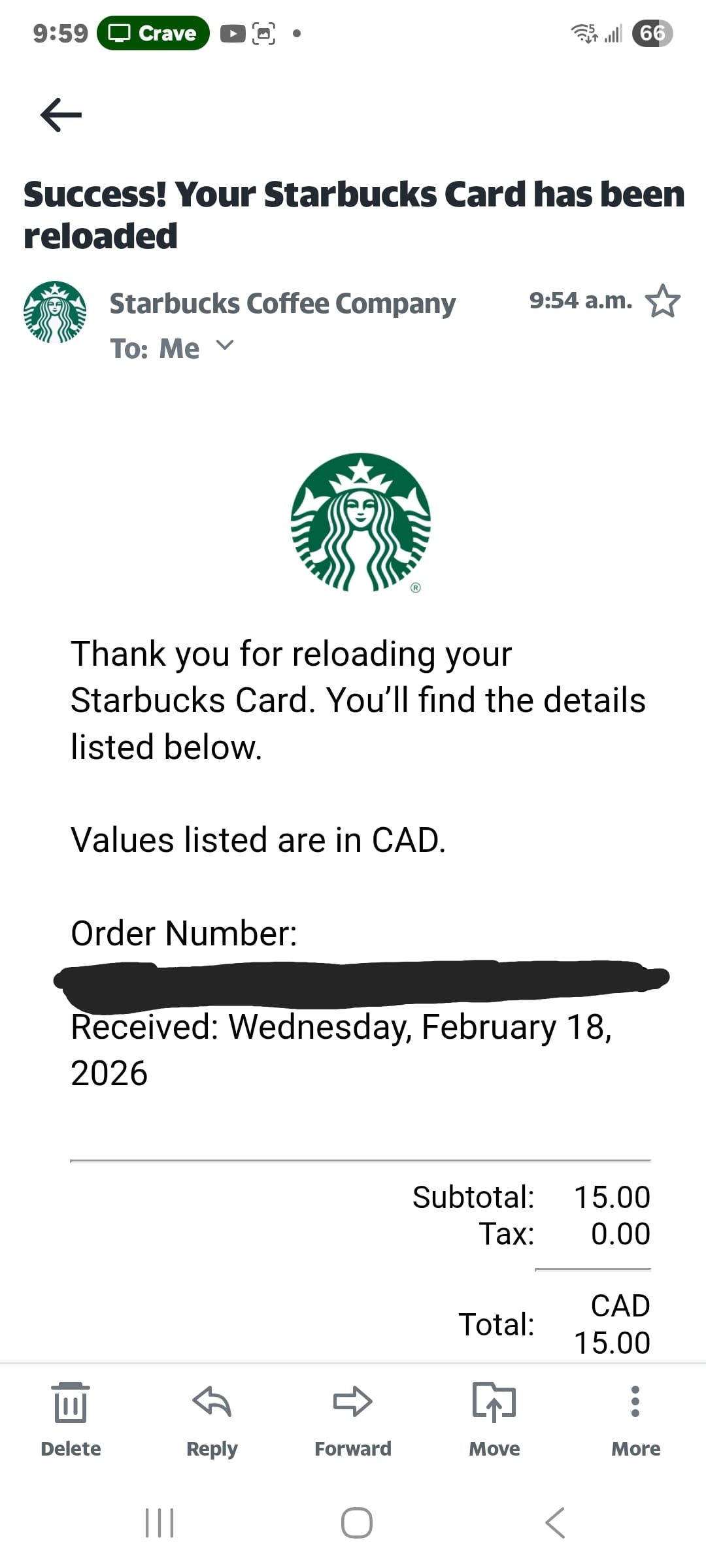

Loading funds was the biggest friction point. Since I’m not a BMO customer, I had to add the card as a bill payment payee through my Tangerine account. I “loaded” the card by making a $25 “bill payment.” The funds took about 3 days to appear. The transaction history later showed a posting date that didn’t align with when the money was actually available, and the app was slow and clunky.

After the $9.99 annual fee was deducted, I was left with a card balance of $15.01. I did not want to leave the house and waste gas or shoeleather on such a useless card. So I tested it by loading $15 onto my Starbucks app so that I at least get some rewards that way. It took a second to add the card to my app, and the transaction was instant.

None of these prepaid reloadable credit cards can replace my daily-use Tangerine Mastercard, but two have earned a permanent spot in my wallet. I will continue to use the Neo Money Card for its aggressive bonus cashback offers. Plus, I love that it has an interactive map of Neo partners that helps me find and support great small local businesses. That’s actually how I discovered my favourite restaurant in Winnipeg.

And I’ll for sure keep Wealthsimple for its free ATM withdrawals. This feature alone solves a major painpoint for me. I no longer have to travel an hour round-trip to withdraw cash from my Tangerine account through a Scotiabank ATM.

If there is one card I’d like to set on fire, it’s the BMO Prepaid Mastercard. It’s the only one in the group that charged me an annual fee, then had the absolute audacity to offer no rewards. Thank you, next.