I wanted to know more about how pawn shops actually worked, so I decided to run a small experiment. I pawned my bass guitar to find out how much cash I could get, what the fees would be, how long I would have to wait to get my guitar back, and whether pawning is ever worth it.

Before we get into it, here’s one important disclaimer: I live in Manitoba, so the rules I had to follow may be different where you live, but I’ll let you know how things worked for me. Pawn shop rules can vary by province, or even by city, so your experience could look a little different.

Get a $60 welcome bonus by signing up for any secured Neo Mastercard using the button below.

* Limited-time offer. Only valid for new Neo customers who open their first eligible Neo credit product and make a purchase within 90 days. Limit of one offer per customer. Offer is subject to the Neo Rewards Policy and may be amended or cancelled at any time without notice.

Also, I’ll admit something slightly embarrassing.

Before this experiment, I didn’t really know what a pawn loan was.

I always assumed pawn shops were just places where you could sell your stuff for quick cash or hunt for deals on used electronics and instruments. Turns out, that’s only part of the story.

There’s a difference between pawning and selling

If you’re like me and never fully understood pawn shops, here’s the simple version.

Pawning means taking out a short-term cash loan using an item you own as collateral.

You bring in an item, the pawn dealer assesses its value, and then offers you a loan based on a percentage of what they believe they could resell it for, typically around 20% to 25% of resale value.

The pawn shop holds your item for the loan term, usually 30 days. To get your item back, you have to repay the amount you borrowed, plus any fees, before the term expires.

If you don’t repay the loan, the pawn shop keeps your item and sells it for its full resale value.

What types of items can you pawn?

For this experiment, I pawned my Fender Precision Bass guitar, which I purchased used for around $500, from Long and McQuade, many years ago. But while I was at the pawn shop, I asked them what kinds of items they typically like to see.

Without hesitation, the answer was: “Anything gold or silver.”

That only makes sense, precious metals are easy to value and resell.

Beyond that, they said that popular pawn items include name-brand power tools, especially Milwaukee and DeWalt, newer electronics like gaming systems, smartphones, and laptops, big screen TVs, and quality musical instruments.

They didn’t provide me with a specific minimum value but explained that they typically lend only 20–25% of the resale value. So if your item is worth $100 or less, you probably won’t get much cash for it.

My experience pawning my bass guitar

I chose my Fender Precision Bass because it’s worth $400-$500 and is in nice condition, but I rarely play it, so I could live without it for a few weeks.

I visited Regent Pawn in Winnipeg’s Transcona neighbourhood, a long-standing shop that was easy to access.

I walked in with my guitar and asked if I could pawn it. I pulled it out of its case, and the store clerk called another employee, I think he was the manager, over. He examined my guitar and then looked it up on his iPhone. I assume he was checking resale values or manufacturing details, since guitar prices vary depending on where they’re made.

The store clerk then asked me how much cash I wanted to borrow.

I hadn’t even considered that part, so I replied, “Whatever you’ll give me.”

After a moment, he said, “How about $100?”

I said, “Sure, sounds good to me.”

How the pawn loan worked

While the clerk was writing up the ticket, I asked about the rules.

I had 30 days to pay back the $100, plus a $30 fee. I could have picked up my guitar and repaid the loan before 30 days, but because this was my first pawn transaction, I was required to wait at least 15 days before picking it up.

The employee pointed to a sign posted on the counter. It referenced a City of Winnipeg bylaw and explained that pawn shops must report items to police and hold them for 15 days. They weren’t technically buying my item, but I guess the same rules applied to pawning.

He mentioned that repeat customers can sometimes retrieve their items sooner.

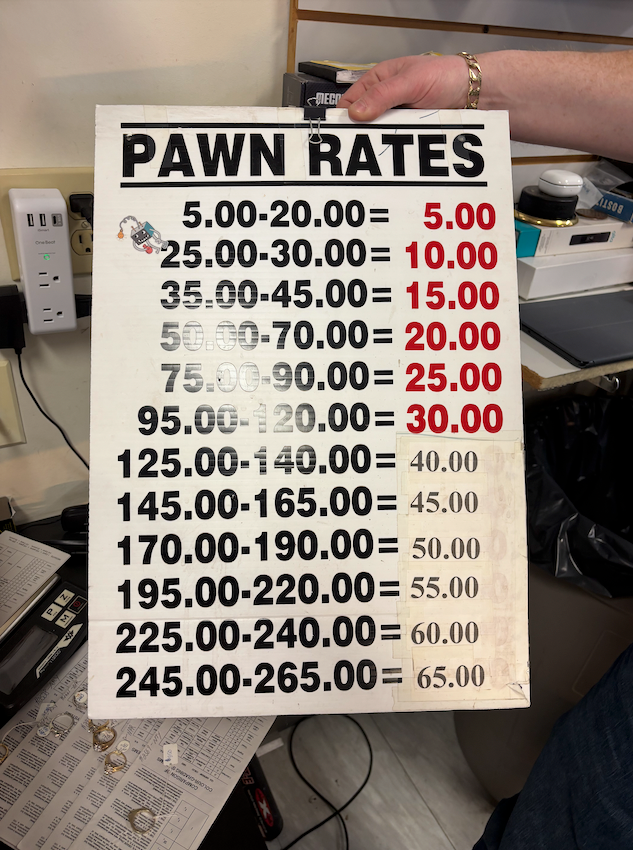

I then asked about the $30 fee. He showed me the following pawn rate table:

Because I borrowed $100, my fee was $30.

As you can see in the image, rates dropped slightly up to $300 borrowed, but above that, I was told the cost was $30 per additional $100 borrowed.

I asked him if the fee would be reduced if I repaid the loan early, say, after 15 days. He said that no, the fee wouldn’t change.

If I didn’t return to pick up the item after 30 days, the pawn shop could list it and sell it for whatever they could get, keeping the proceeds.

When I was finished asking questions, the clerk handed me two $50 bills and my receipt, and my bass guitar stayed behind.

Waiting period

As mentioned, I had to wait at least 15 days before I could reclaim my guitar. It actually worked out well, since I had a 10-day trip to Ottawa during that time.

A few days after returning home, I went back to the pawn shop.

Getting my guitar back

I went back to Regent Pawn 16 days after dropping off my bass, and I told them I was there to pick up my guitar. They brought it out from the back room, I handed over $130 in cash ($100 loan + $30 fee), and they returned my bass.

They also kept my original receipt.

I should point out that Regent Pawn strongly prefers cash repayment. I was told that debit cards are accepted, but credit cards are not.

The real cost of the loan

The process of pawning my guitar was very smooth, but it was also very costly. On the surface, borrowing $100 and paying back $130 doesn’t sound too complicated.

But when you look at the $30 as interest, the picture changes quickly.

I paid $30 to borrow $100 for 15 days, which works out to a 30% borrowing cost over just two weeks.

If you stretched that same cost over an entire year, the equivalent annual interest rate would be roughly 730%!!

To compare, a typical credit card charges about 20% – 25% annually. Many high-interest personal loans fall in the 30% – 40% range. Even payday loans, which are heavily criticized for their high costs, have a maximum fee of $14 on a $100 loan in Ontario. That’s cheaper than my pawn loan.

In other words, pawn loans are extremely expensive when viewed as interest, even though their flat-fee structure can make them seem simpler or less intimidating up front.

Comparing local pawn shops

After paying off my pawn loan, I called a couple of other local pawn shops to see how their rates compared to Regent Pawn's. And yes, they were very similar.

Both shops, City Pawn and Sales, and Broadway Pawn and Sales Ltd., told me that they charge 30% interest on whatever you borrow (so, $30 on $100), and will lend 20% of the current retail price of the item you’re pawning, for a maximum of 30 days.

Is pawning ever a good idea?

Pawning can make sense in a few specific situations.

It can provide fast access to cash when you need short-term liquidity and don’t qualify for traditional credit. Because the loan is secured by an item rather than your credit score, it may be an option for people with bad or limited credit.

Compared to payday loans, some borrowers may also prefer pawning because there’s no risk of debt collection. If you can’t repay, it won’t affect your credit score or bank account… You simply lose the item.

But there are clear downsides.

Pawn loans can become very expensive when used repeatedly or for extended periods. They’re also a poor choice for items with emotional value, since failing to repay means permanently losing a personal item you may value.

And relying on pawn loans regularly can quickly turn into a costly borrowing habit.

So… was it worth it?

Would I do it again? No, even though I had a very smooth experience.

It was just too expensive. Paying $30 to borrow $100 for just over two weeks is far costlier than almost any traditional form of credit.

Better alternatives include using an emergency fund, a line of credit, or even a credit card if you can pay it off quickly.

That said, the experience helped me understand why pawn loans exist. They offer something many lenders don’t… instant cash with no credit check and minimal paperwork.

The bottom line?

Pawn loans offer quick cash, but at a steep price.