I don’t know about you, but in the middle of a long Canadian winter, I start dreaming about ways to stay warm. Escaping to a sunny southern destination is usually the first thing that comes to mind. But during a particularly cold January here in Winnipeg, I caught myself thinking about something a little closer to home… how nice it would be to soak in my own hot tub, right outside my back door.

But I know very little about hot tubs, so I decided to visit a local hot tub retailer to learn more. I walked into Krevco Lifestyles in Winnipeg on an absolutely frigid January afternoon with one goal. I wanted to find out what it actually costs to finance a hot tub in Canada.

Hot tubs are not cheap. In fact, they’re even more expensive than I realized. According to the salesperson I spoke with, the typical starting price is around $16,000, and prices can go up to $30,000 or more.

He mentioned that the lowest-priced tubs they sold were around $13,000, but that they were pretty small and not very popular. I didn’t see any of those on the sales floor.

Here’s what I learned, and why financing a hot tub is probably not a good idea.

In-store hot tub financing

Krevco Lifestyles (and apparently many other hot tub retailers) use Financeit for their in-store financing. I asked the rep to break down the cost of financing a hot tub with a $16,000 purchase price, since I was told that was a typical starting point for many buyers.

To keep things simple, I’m not factoring taxes into the equation. Here’s the math he showed me

A few things jumped out at me.

First, the rep mentioned they can extend these loans to 20 years (240 months), as shown in the example above.

That’s shocking for something like a hot tub.

What’s even more shocking is that if you chose the 20-year payment option, you would end up paying almost $30,000 in interest, and over $45,000 (for a $16,000 hot tub) by the time the loan was paid off.

By the way, that lower “intro” payment was a temporary promotion designed to make the deal feel manageable. But once the 0% period ends, the real cost kicks in.

Here is the payment over 5 years

Now, you don’t have to choose the 20-year option. If you financed the same $16,000 over 5 years, your monthly payment would be roughly $365, the total interest paid would be around $5,900, and the total cost of the hot tub would be around $22,000.

It’s a lot less than the 20-year scenario, but it’s still nearly $6,000 in interest on a backyard luxury item.

Other ways to finance a hot tub

As you can imagine, those high interest costs had my head spinning as I left the hot tub store. I wasn’t seriously in the market for a hot tub, but the experience made me think about other financing options.

Take out a personal loan

If you qualify, an unsecured personal loan from your bank might run somewhere between 9% and 12% or more, depending on your credit profile. A line of credit could be similar, often prime plus a few percentage points.

Let’s say you qualified for a 9% personal loan for five years on $16,000. Your monthly payment would be about $332, and your total interest cost would be close to $4,000.

That’s cheaper than in-store financing, but still almost $4,000 in interest.

Now, if you can’t qualify through a bank, you could try a financing company like Easyfinancial or another alternative lender. But that’s where things can get dangerous.

Rates at these lenders can run 20% to 30% or more. At 29.99% over five years, you would be looking at a monthly payment of around $515, and around $15,000 in interest over five years.

That’s nearly doubling the cost of the hot tub.

I recently wrote about how to find personal loans through an app called Smarter Loans right here on MooseMoney, and the same rules apply here. High-cost lenders should be an absolute last resort, especially for non-essential purchases.

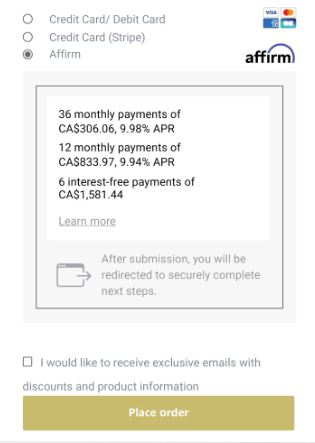

Financing With a BNPL Company Like Affirm

I found one Canadian hot tub company (there may be others) that offers Buy Now Pay Later (BNPL) financing through Affirm.

BNPL lets you take something home right away and pay for it over time instead of all at once. Usually, the cost is split into smaller payments, sometimes with no interest at first, but if you don’t pay it off within the promo period, interest or fees can kick in pretty quickly.

The screenshot below shows the Affirm financing option published on the hot tub company’s website (for a different purchase price). The interest rates look pretty good, but the fine print at the bottom of the page stated that Affirm’s interest rates range from 0% to 31.99% APR.

BNPL financing can offer short-term 0% promotional financing, along with fixed payments, but the interest rates can be very high if you take longer to pay.

BNPL can feel psychologically easier because it’s broken into neat, predictable payments. But the math doesn’t magically change.

Putting It on a credit card (please don’t)

Could you put a hot tub on a credit card with a high enough limit? Technically, yes, but should you? Absolutely not.

Standard Canadian credit card interest rates can range from 19.99% to 24.99%. Let’s say you financed $16,000 at 19.99% and paid it off over five years. You would pay about $425 per month and end up paying over $9,000 in interest.

But that assumes you’re disciplined enough to actually pay your credit card off in five years. The danger of a credit card is that you can reborrow against the credit limit. Many people end up paying much longer, which means even more interest.

Credit cards are one of the most expensive ways to finance any purchase. And if your income drops or an emergency hits, a huge balance could quickly become a serious problem.

Paying with cash

So, what’s the cheapest way to buy a hot tub? With cold, hard cash from your savings account. You won’t be charged any interest, and you won’t have a monthly payment hanging over your head for years.

That said, just because you can pay with cash doesn’t mean that you should. Before shelling out $16,000 on a luxury item like a hot tub, ask yourself the following: Am I pulling money out of my emergency fund? Do I have high-interest debt I should be paying off first? And, will making this purchase delay other financial goals?

Remember, a hot tub is not a necessity. It’s a lifestyle upgrade. And lifestyle upgrades should never come at the expense of your financial stability.

Another option worth considering is buying used. The sales rep at Krevco told me the shell of a hot tub can last decades. It’s usually the pumps, jets, and components that need replacing. A used unit could cost a fraction of new, especially if you’re comfortable budgeting for maintenance.

What about the other costs of owning a hot tub?

There are other costs to consider before you buy a hot tub, which is something many people overlook. I did some research online and found that most hot tub owners in Canada should expect to spend roughly $60 to $120 per month to operate their hot tubs. Electricity is usually the biggest expense, and can average $30 to $70 per month, or more to maintain the temperature year-round. Obviously, the costs will be higher in colder climates. Water care and chemicals can add another $20 to $40 per month, and routine maintenance, such as filter replacements, cleaning supplies, and minor repairs, can average $500 to $1,000 per year. And over the years, you can expect to replace major parts, such as pumps or heaters.

So… Is Financing a Hot Tub Worth It?

After running the numbers, here’s my conclusion:

Financing a hot tub is expensive, no matter how you slice it. Even at “reasonable” interest rates, you’re looking at thousands of dollars in borrowing costs. And while stretching out the term over several years can lower the monthly payment, you’ll pay far more in the long run.

If you really want a hot tub, I recommend saving for it, paying in cash, and even buying a used one.