I used my Neo Money prepaid card exclusively for a week and then switched to EQ Bank's prepaid card for another week. The experience with both cards had its ups and downs, but I will keep Neo for groceries and gas and EQ for the rest.

These cards are different

Neither the Neo Money card nor the EQ Bank card is a regular debit card because you earn cash back on purchases. They are not credit cards either because you're not borrowing money at a prescribed interest rate. Still, you can earn cash back with nearly every swipe, tap or mobile wallet transaction. That makes your money go further.

Even though I spent more on my EQ Bank card, I still walked away with 38% more cash back with Neo.

A cash back refresher

Before diving into EQ vs. Neo, you have to understand cash back. The Neo prepaid card and the EQ Bank prepaid card give you back a percentage of the money you spent during the month. It gets deposited on your card to spend or you can transfer it to your chequing account.

Calculating your cash back is not hard. Most cash back rewards are based on a yearly spend.

Let's say you buy $100 in groceries. If you get 0.5% cash back on groceries, then the calculation is as follows:

- Convert 0.5% into a decimal by dividing 0.5/100=0.005

- Multiply $100 x 0.005=$0.50.

That is your cash back.

My cash back haul from EQ vs. Neo

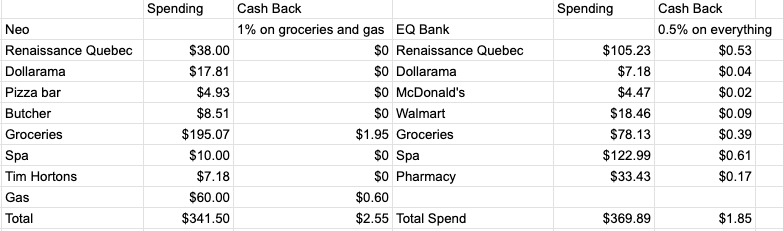

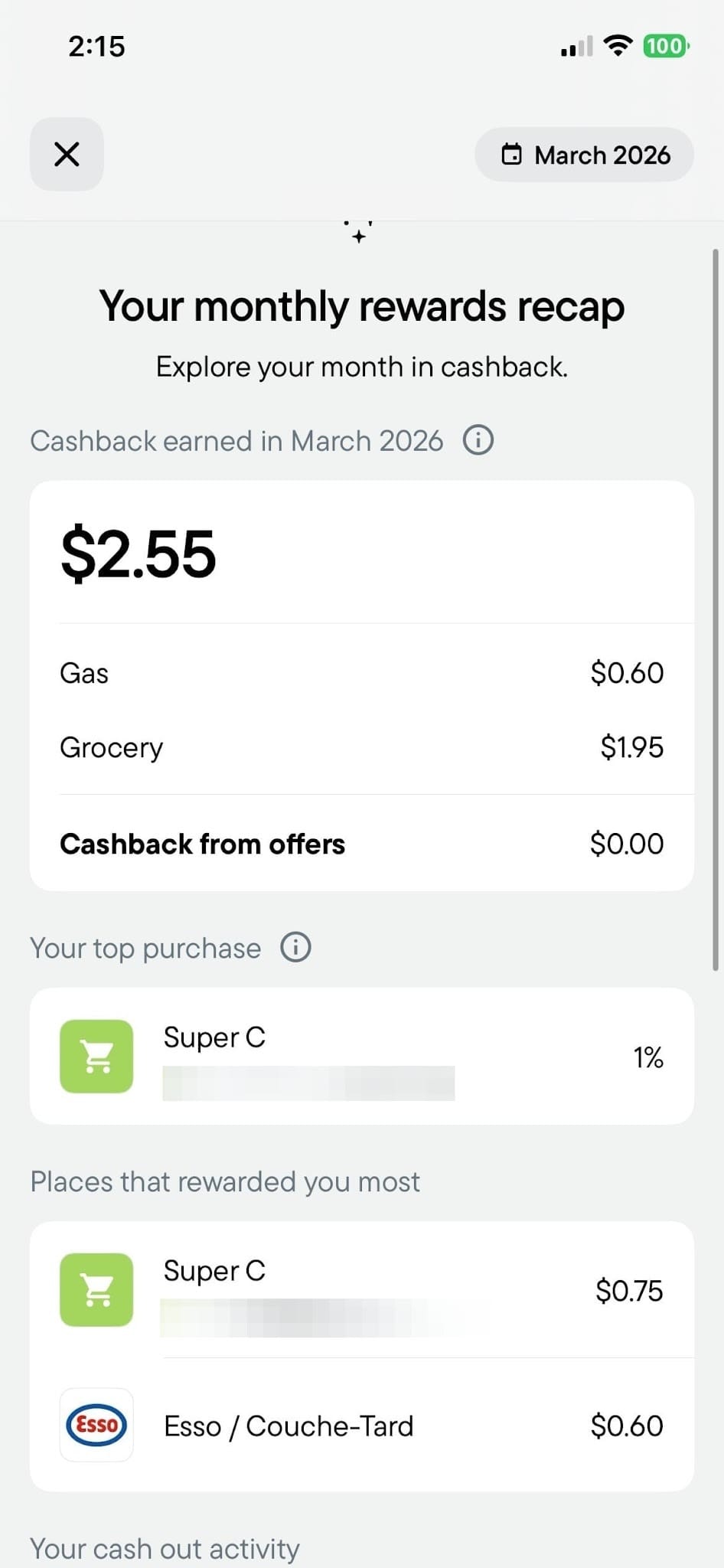

The potential cash back from Neo depends on where you spend your money. You can get 1% back on groceries and on gas, but that's it. You can also earn rewards when you shop at Neo partners. I spent a lot on groceries and bought gas, which netted me $2.55 in cash back.

EQ Bank is much more straightforward: you earn 0.5% on everything and there are no partnership hoops to jump through. I did not buy gas with my EQ Bank card, but I spent more than I did with Neo. My cash back will be $1.85.

You need to open a chequing account to get the cards

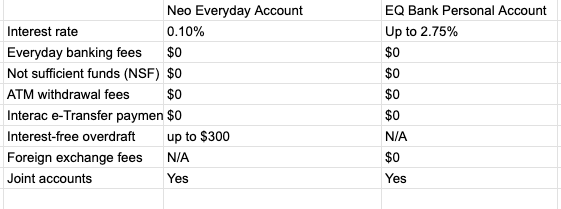

The Neo card and the EQ Bank card are tied to chequing accounts at the respective banks. Here is a breakdown of the basic advantages of each account.

Both the Neo prepaid card and the EQ Bank card work everywhere they accept Mastercard. Since it is a prepaid card, you load it with money from your accounts.

Once you open your account, download the bank's app to track your money and spending.

The Neo sign up process

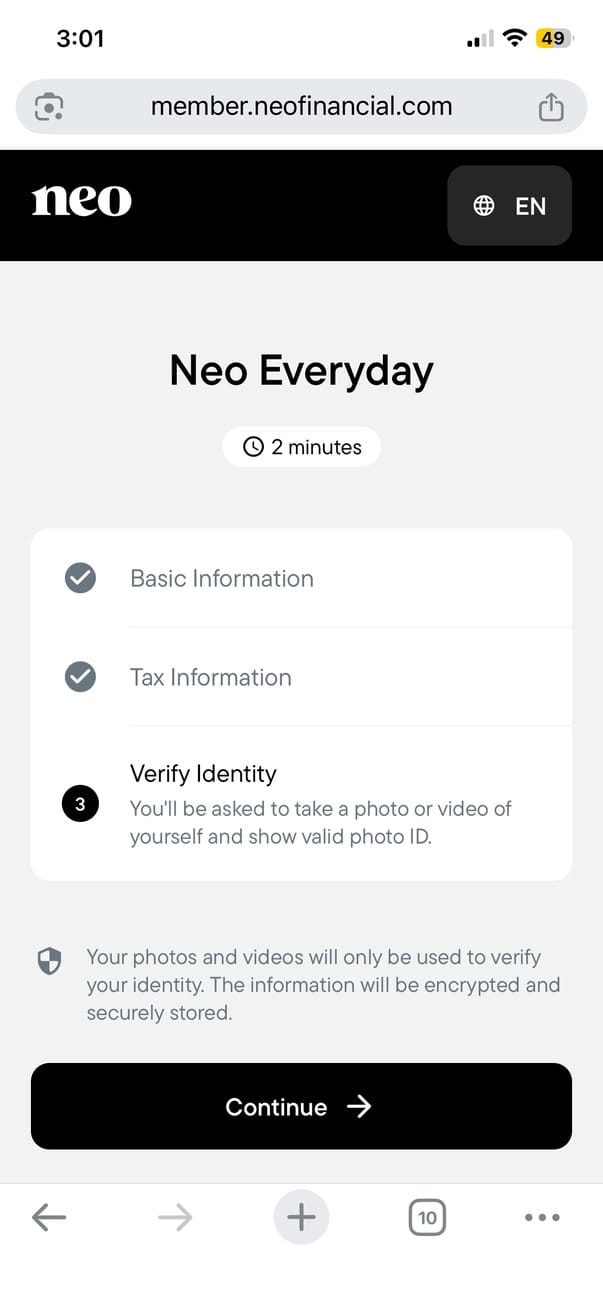

First, they ask for your email address and send you a verification code. Once verified, they ask you what you’re looking for.

Next, they ask you standard questions to verify your identity:

1.Provide your full legal name, date of birth, address and how long you’ve lived there, and your employment status.

2. Supply some tax information: they ask for your Social Insurance Number or SIN and whether you pay taxes outside of Canada.

3.Verify your identity: this includes a selfie and a piece of photo ID.

The entire process was smooth.

Now time to put money into your account. I chose to link it to my current financial institution, but I could have used Interac e-transfer as well.

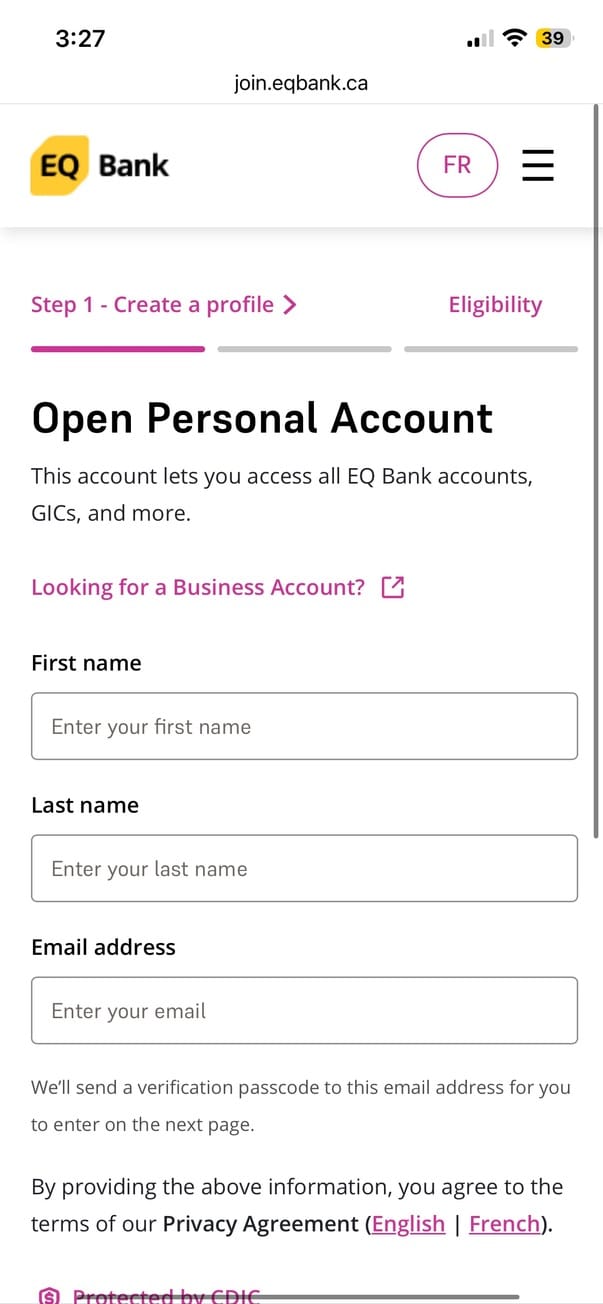

The EQ Bank sign up was also hassle free

The sign up was the same as for Neo. It requires your first and last name and an email address. It also asks for your mobile phone number to send you a passcode. Next, EQ asked for your residential address, date of birth and SIN. It even lists that your credit score won’t be affected by signing up.

At sign up, EQ Bank stated that the money could be available to load to my virtual card within 4 business days - a full day ahead of Neo.

EQ asked how I want to use the account. The options were:

- Personal savings

- Deposits and living expenses

- Investment

Investments? That screams established, if not future focused.

Once I set up my password, it was a few seconds until EQ verified my account.

Getting the physical cards was fast

Both Neo and EQ Bank’s cards arrived within a day of each other, and I had both of them within 2 weeks.

Neo came in an envelope. It was simple. Then came the EQ card.

EQ card's packaging made me feel elite. It was gorgeous and the message reminded me about the advantages of using the card. Is that why EQ Bank only gives 0.5% cash back on purchases? Probably not.

Your money is not available immediately

I had to wait for the money to become available at both banks. It took about 7 days before I could actually access and use the cash in my new accounts.

If I needed to spend money earlier, I would have to use my regular bank’s debit, cash or a credit card. Once the money cleared I was ready to go shopping.

Shopping with my Neo card

I put $500 on my Neo card and my first purchase was a fill-up at a gas station. I spent $60 and got a nearly instant notification and email about the purchase plus how much cash back I earned. The dopamine kicked in and I was in love with my Neo card.

Why didn’t the tap work?

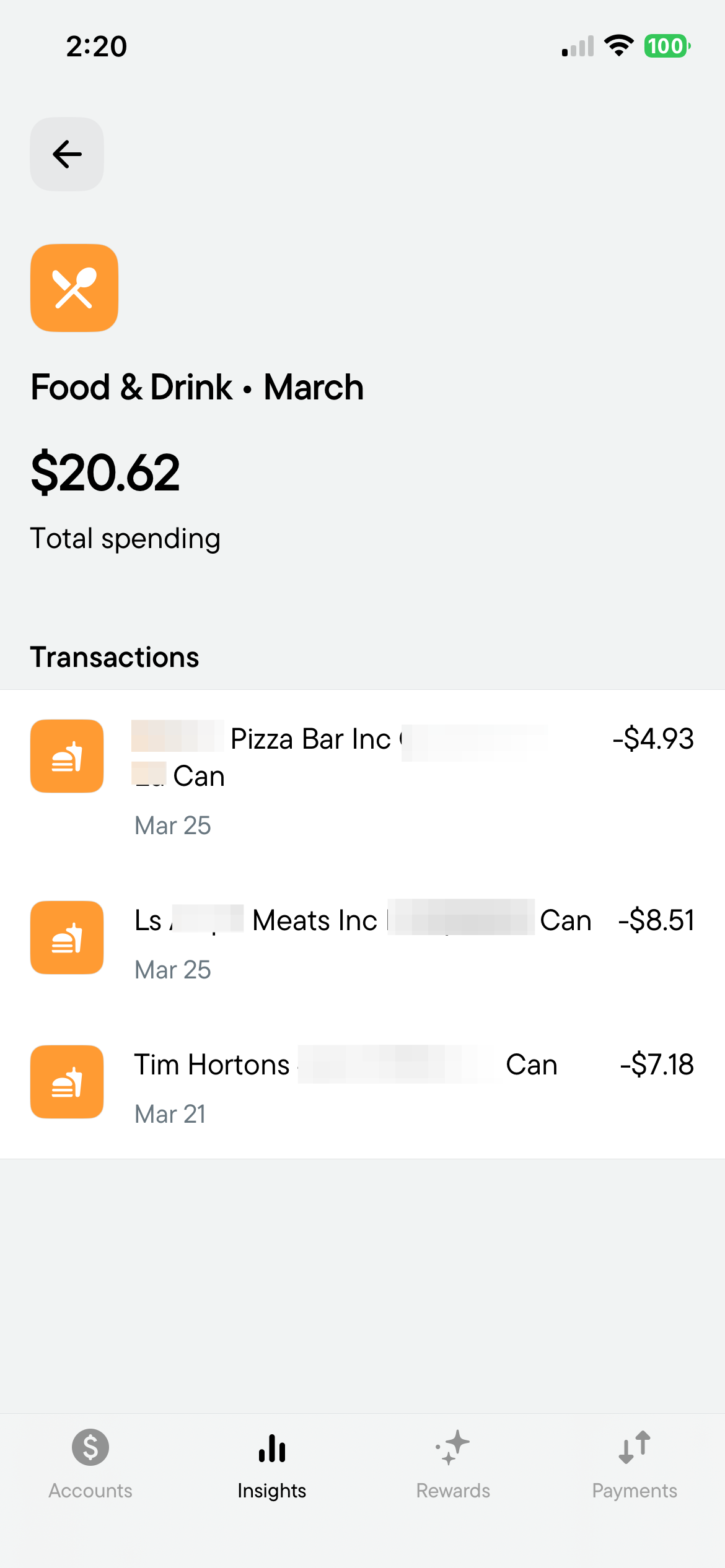

There I was at the self-checkout trying to buy groceries. I tried paying with tap but it didn't work. Nothing happened. The bill was $195, so I assumed that was why had to insert my card to pay.

I moved on to a local butcher because the meat department at my local grocery store was picked over. The bill was $8.51 and I tried to tap again. It still didn't work. I was getting mildly frustrated with the card.

Sometimes your groceries only count as Food & Drink

Neo's cash back seemed to favour big grocery stores for cash back. It didn’t give me any cash back at smaller food stores or variety stores that also sell groceries.

For example, my butcher was classified as a Food and Drink transaction instead of Grocery. My Dollar Store purchase was labeled as generic Shopping, even though the store sells groceries.

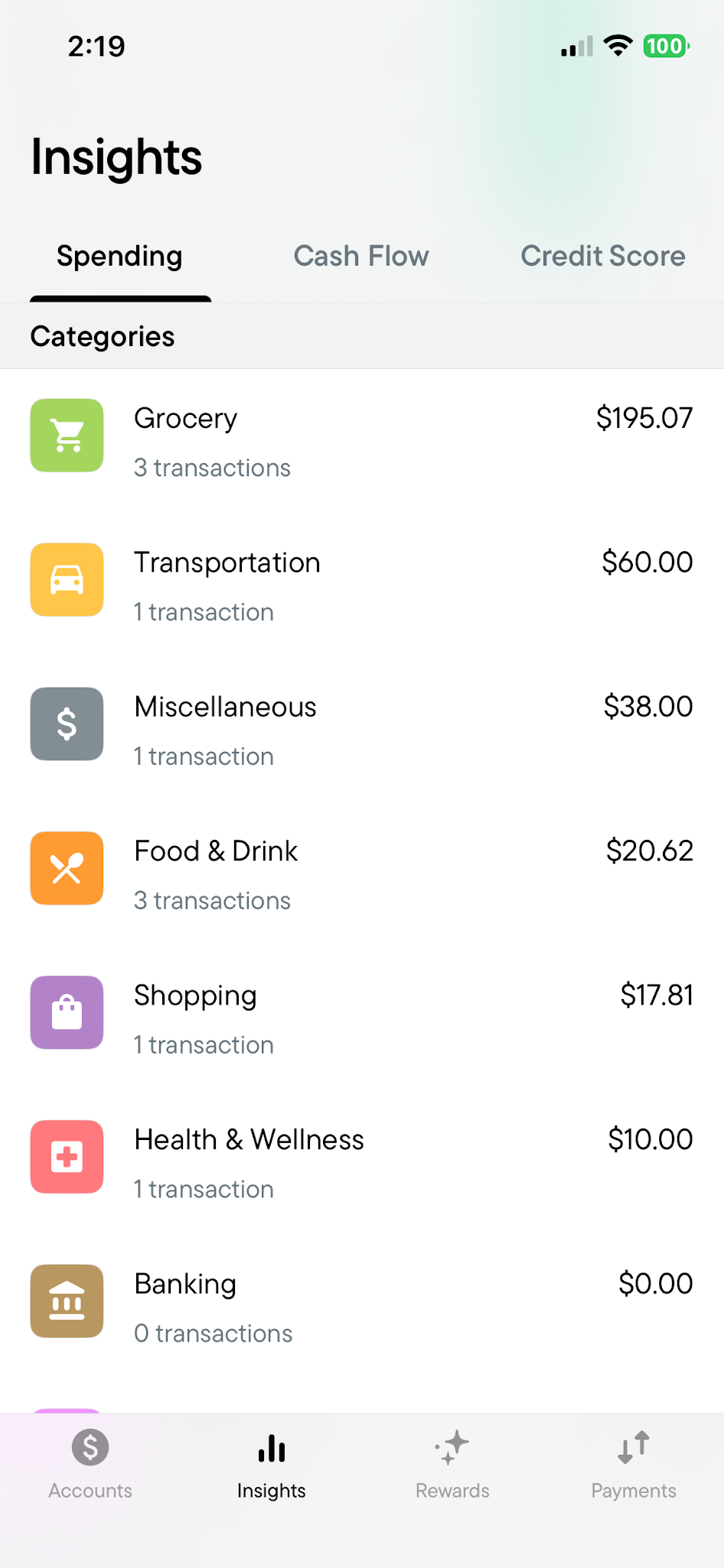

Finding my $2.55 cash back in the Neo app was easy

At the end of the week I checked my earnings in the app’s Insights feature and was pleasantly surprised. Neo showed my total spending and my cashflow. There was even a tab to get my credit score.

I could easily cash out those dollars back to my Neo Everyday account. As for my 0.10% chequing account interest? It gave me a nice $0.02.

Let’s go shopping with my EQ Bank card

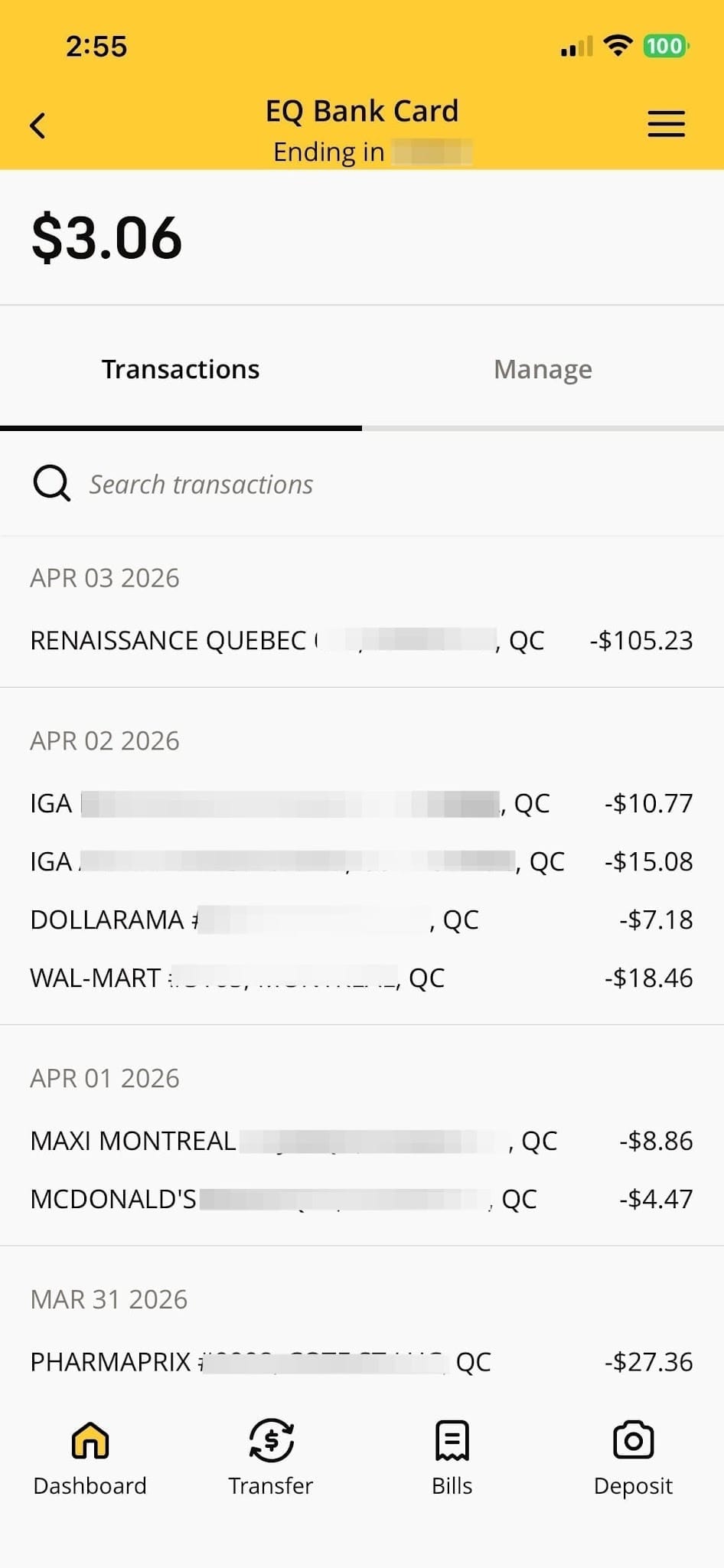

I put $500 on my EQ card and spent $369.89 which is $28.39 more than I spent with Neo.

I had a lot of food to buy during my Neo week, but less during my time with EQ Bank. I didn't buy gas with my EQ Bank card either.

However, EQ Bank had no restrictions on where I could earn my 0.5% cash back. I bought groceries at Wal-Mart, shopped Dollarama and went to the pharmacy. These are all purchases that potentially would not earn me any cash back with Neo.

The tap that always worked but less informative notifications

I went shopping and only had to use the tap. It always went through.

I got notifications when I used my card but it was not as detailed as Neo's. EQ would tell me how much I spent but I had to log in to the app to get more details. It was not as much fun as a Neo notification.

It was not as easy to get my cash back with EQ Bank

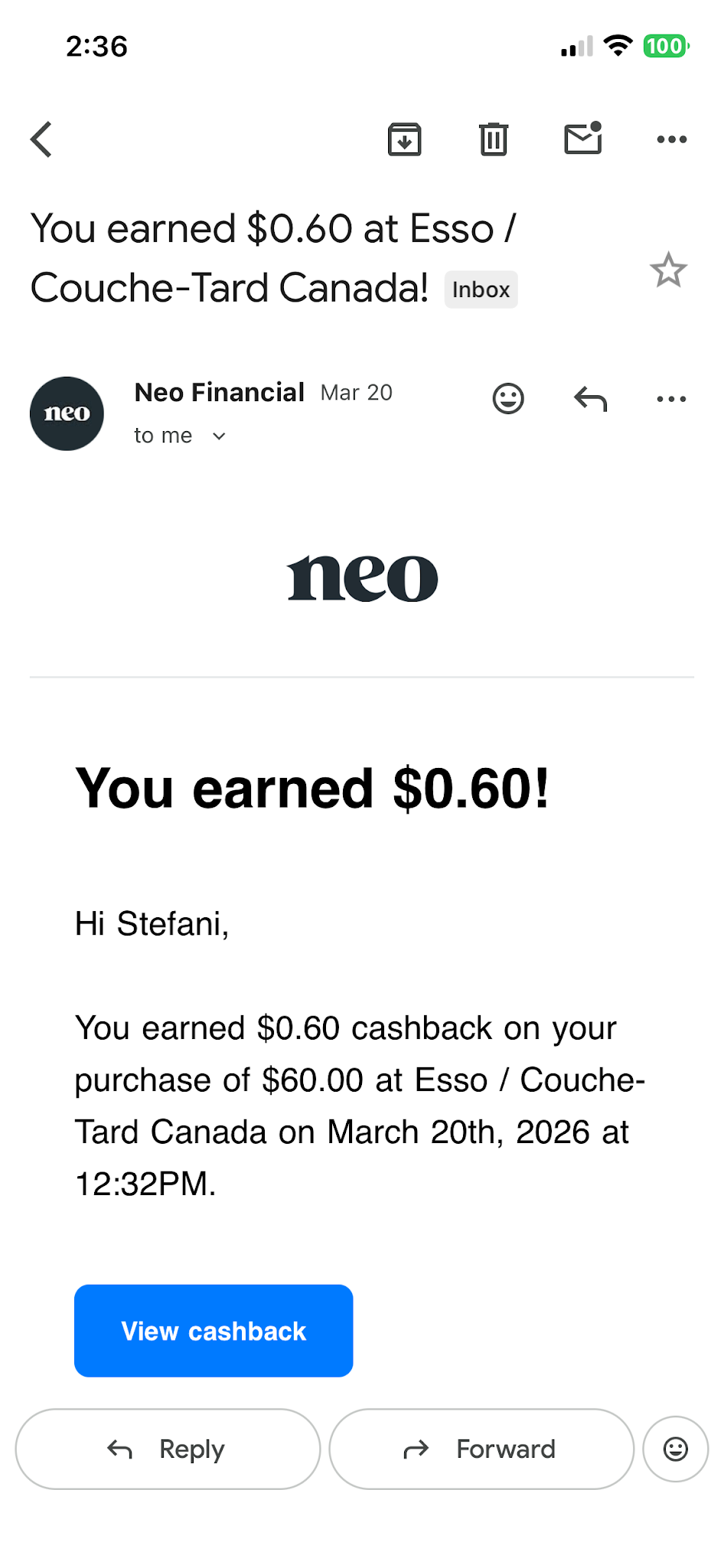

I used my EQ card for one week starting in late March and into the first week of April. I was so excited to see how much cash back I would earn. When I did not see any cash back by April 7, I contacted Customer Support.

They were outstanding. They walked me through how they calculated my interest of $0.27 and explained that there was probably a lag in the back end processing of my cash back. They said that it might be there in the next few days or to wait until the April statement.

I waited nearly three weeks and didn't get all my cash back

On April 17th I got the notification that some of my March cash back was now on my EQ card. A wonderful $0.61 was ready for me to spend. I will gladly take it, but the problem is that they owe me more.

Settlement dates are not the same as transaction dates

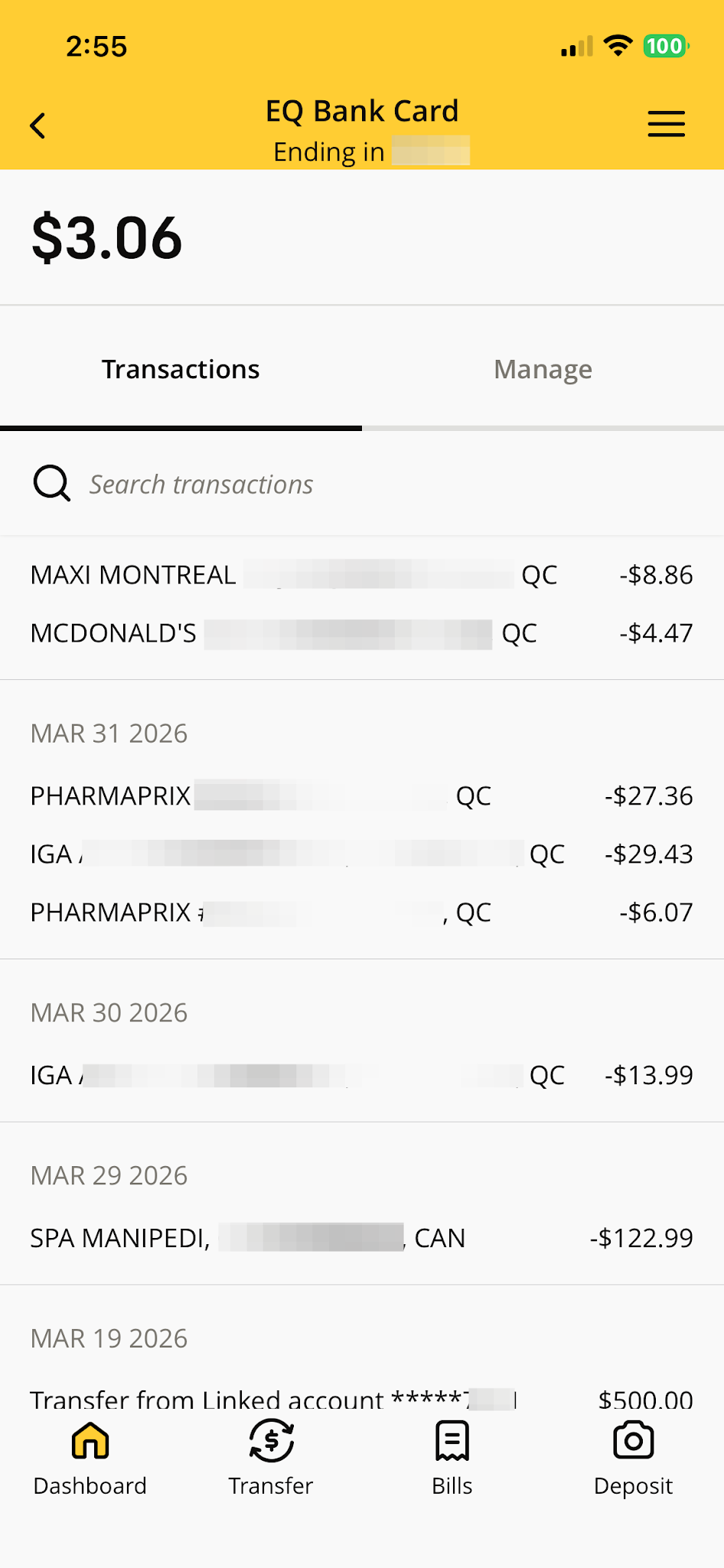

I again called the phenomenal EQ Bank Customer Support. I was again treated so well. It turns out that only my spa splurge of $122.99 was included in my March cash back, and that equals to $0.61.

My other March transactions only settled in April. That means that the remaining $246.90 will earn cash back for my April statement. If all goes according to math, I will get $1.24 in cash back.

I earned 38% more cash back with Neo, but it's not the whole story

So, let's say that settlement dates didn't crash the party. EQ Bank would have paid me $1.85 in cash back for my total one week spend. That still doesn't beat the $2.55 I got from Neo for spending less overall, but more on groceries and gas.

What if I had spent the same money the same way on each card?

What if I spent the $341.50 in the same categories that I did with Neo but used my EQ Bank card? It turns out that my cash back would be $1.71, and Neo still wins.

How EQ Bank can come out the winner

Let's flip it the other way. What if I spent the same amount on groceries as I did with EQ Bank but put it on my Neo card? Well, if I spent only $78.14 on groceries instead of $195, my overall cash back would be drop to $1.38 including my gas. In that scenario, EQ Bank's $1.85 cash back easily wins.

How to use both cards to get even more for your money

The moral of the story is that you have to look at your overall spending to maximize your cash back. If your biggest spend is always on groceries and gas, then the card with higher cash back rate is the best option.

The best idea might be to use Neo for your groceries and gas and the EQ Bank prepaid for everything else. With no minimum balance required for either chequing account, there is no obvious downside to having both.

EQ vs. Neo: Which is best for you?

Neo Financial and EQ Bank are both legitimate Canadian financial institutions but that doesn't mean that they are marketed the same way.

Neo Financial, which is known for its secured card, seems like a good match for people trying to establish themselves from young adulthood to the point where they would need to manage a business or a downpayment. Plus, it's 1% cash back on groceries and gas is compelling for anyone.

EQ is more aggressively trying to get your entire financial portfolio, and it seems like they assume that you are at a more advanced life stage. They don't offer secured credit cards like Neo, but they do offer Tax Free Savings Accounts (TFSA), First Home Savings Accounts (FHSA), the option of a US bank account or a business account.