“He lost the use of his back legs,” said H. Guiterrez. “By the next morning, he was struggling to breathe.” Four years ago, my neighbour rushed her Bichon-Shih-Tzu puppy to the vet. His daily play sesh with the family cat left him with a broken back. Gutierrez was forced to choose between a six-hour drive to a specialist for an expensive, high-risk spinal surgery or euthanasia.

With no room on her credit card and an emergency fund already depleted by other financial curveballs, she didn’t know vet financing options were even a thing. Her family had to make a decision that still hurts to talk about.

Jack’s story inspired me to find out what options actually exist. So I called 20 Veterinary clinics in Canada to ask about payment plans, financing options, and credit cards. Then I interviewed a Veterinarian to get some budget-saving insight. Here’s what I learned.

Do Vets Do In-House Payment Plans?

It’s so rare that the answer is basically no. Only one vet clinic out of the 20 I called will consider an in-house payment plan, and only under very specific circumstances. Paris Veterinary Clinic in Paris, Ontario, sometimes offers a payment plan to longtime clients if their pet needs urgent or unexpected care.

It is not available for planned, routine services like spay/neuter, dental cleanings, vaccines, etc. You have to pay 50% of the cost upfront, with the remainder repaid over three months. They also require pre-authorized payments from your bank account or a credit card number on file.

Credit Cards & Financing Options

All clinics I called accept credit cards and debit cards, with eight clinics not accepting Amex due to higher payment processing fees. And 75% of the clinics accept some sort of third-party financing. Here’s a quick breakdown of the options available at each clinic:

Using a Finance Company

In most cases, the lender pays the clinic directly, and you repay the lender. Here is a list of the top finance companies recommended to me by the vet clinics I called:

Scratchpay

Scratchpay offers 12 or 24-month loans for $200–$10,000, with a required $15 down payment. Rates range from 5.99% to 45.99%, depending on your credit profile, employment, and income information.

Scratchpay doesn’t publish a minimum credit score. Approval is based on factors like credit history, income, and employment. They told me the application uses a soft credit check, so applying won’t impact your score. Once the loan is opened, they report your account and payment history to the credit bureaus, which can affect your credit.

Although Scratchpay’s site advertises 0% plans, a rep told me 0% financing isn’t available to Canadians.

Scratchpay only works with in-network partner clinics, so confirm your vet participates before applying. Clinics also pay a 5% service fee (deducted from what they receive), which may or may not be reflected in pricing.

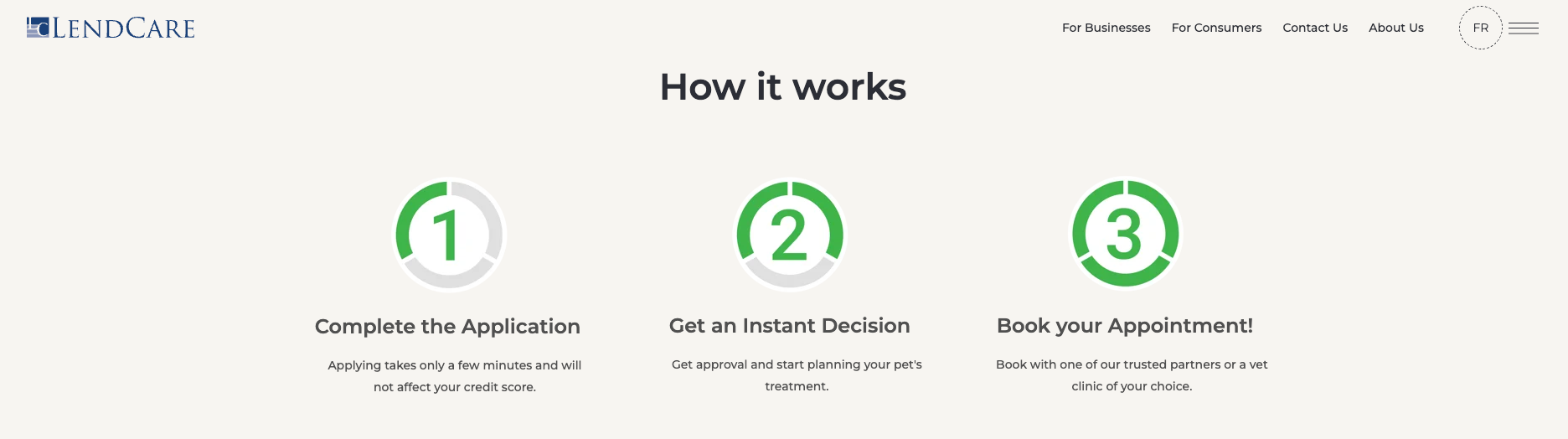

LendCare

LendCare offers loans for $1,500-$15,000 with 1 to 5 year terms and rates ranging from 9.99%–29.99%, depending on your financial profile. If approved, LendCare pays the clinic directly, and you repay LendCare over the term. They don’t disclose a minimum credit score.

Financing is only available through authorized partner clinics. You apply at the clinic, and the clinic runs the credit check, submits your application, and provides a treatment estimate that LendCare uses to confirm the approved amount. LendCare can also refer you to participating clinics in your area.

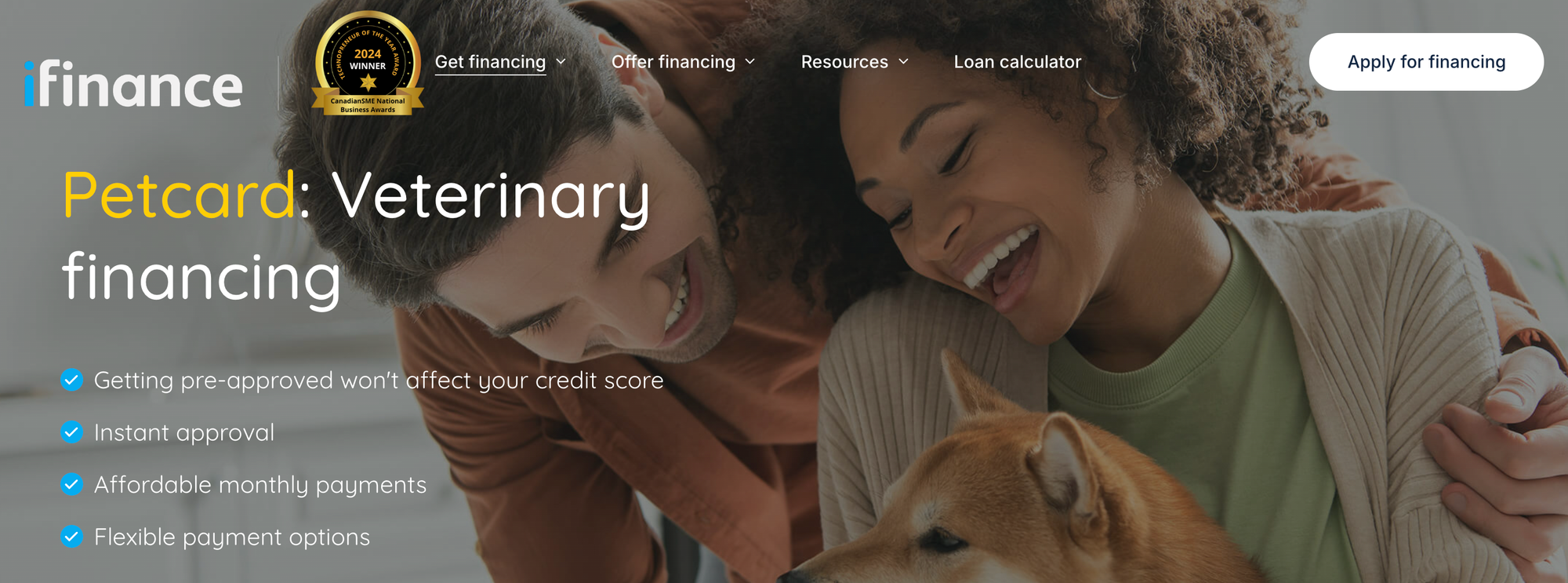

Petcard/iFinance

iFinance previously offered a credit card called Petcard, but that product was recently discontinued. It now offers personal loan financing for $500–$40,000, with 1-6 year terms, and rates ranging from 9.99% to 29.99%, depending on your credit profile.

Like other vet-financing programs, iFinance is generally limited to in-network clinics and eligible services, and the lender pays the clinic directly. They don’t disclose a minimum credit score, but their site provides rate estimates by credit score range, for example:

- 750+ (~9.99%)

- 650–700 (~12.99%)

- 600–650 (~16.99%)

- 525–600 (~19.99%)

You can prequalify without impacting your credit score. In my test, I was prequalified for $2,000 at 14.25% over 5 years. But their customer support sucks. The rep was a bit rude and not especially helpful when I called. She kept telling me to visit the website, even though it did not have the information I was looking for.

Humm

Humm was suggested by my best friend who is a veterinarian. It offers financing terms from 6 biweekly payments up to a 5-year term, with no minimum borrowing amount and a maximum of $30,000. Rates range from 4.99% to 14.99%, depending on the plan and your overall profile.

They do not do hard credit checks for loan requests under $17,500. Approval is based on a soft credit check and your financial profile. But amounts over $17,500 do require a hard credit check and a strong credit history.

Humm does not have a minimum credit score requirement. The rep told me they consider all credit profiles, with more emphasis on things like income, employment, housing status, and ability to repay. A score above 600 greatly improves your approval odds, but lower scores are not automatically declined.

They only work with in-network partner clinics, but their online clinic-search tool was the easiest to use and showed tons of partner vets across Canada. You can either apply on your own through their website, or the clinic can send you an application link.

Of all the lenders I contacted, Humm provided the best customer service by far. The rep was patient, kind, and gave me the most detailed, in-depth answers. Humm offered the lowest interest rates and definitely sounds like the most poor-credit-friendly lender.

Buy Now Pay Later (BNPL) Payment Options

Buy now, pay later (BNPL) lets you split a vet bill into a few smaller payments. Some plans are advertised as 0%, while others charge interest or fees depending on the plan you choose, your credit profile, and financial situation.

A few clinics I called offer BNPL at checkout through Affirm (formerly PayBright) or Sezzle. However, these BNPL providers usually charge the clinic a merchant fee, typically 6% plus $0.30 per transaction. Beware, some clinics may price these fees into the cost of service, while others absorb them.

Affirm (Formerly PayBright)

Three clinics offered me Affirm. However, it was unclear who starts the application. One clinic told me to apply ahead of time, while Affirm support said the clinic needs to initiate it. Confirm the process with your clinic ahead of time. You do not want to be figuring this out in an emergency.

Based on what I gathered, financing may be available for roughly $300 up to $15,000, with rates around 0% to 32%. The 0% offers are typically reserved for borrowers with excellent credit.

Affirm doesn’t disclose a minimum credit score. Approval depends on your overall credit file and other underwriting factors.

Sezzle

Only one clinic I spoke to offered Sezzle, and that was Novel Veterinary Clinic in Burlington, Ontario. They said Sezzle is no credit check with guaranteed approval, no minimum purchase, and financing up to $2,500. Repayment is typically interest-free, often over six biweekly payments.

The clinic suggested setting up a Sezzle account in advance, but completing the BNPL process in-clinic so staff can help.

The clinic said Sezzle doesn’t charge them fees, but Sezzle’s merchant terms indicate merchants are typically charged 6% plus $0.30 per transaction. If you plan to use Sezzle, ask your clinic whether they absorb that cost or build it into pricing.

The Farley Foundation: A Vet Care Subsidy Program

The Farley Foundation is an Ontario charity that helps low-income pet owners cover the cost of unexpected vet care when your pet is sick or injured. It can help pay for things like diagnostics, hospitalization, and surgery. But it does not cover routine stuff like vaccines, regular checkups, food, spay/neuter surgeries, etc.

Eligible people include those on the Guaranteed Income Supplement (GIS), Ontario Disability Support Program (ODSP), Canadian Pension Plan (CPP) for disability, Ontario Works, households with annual income under $35,000, and some senior/care facilities with live-in pets. To get help, the vet has to apply on your behalf (you can’t apply yourself). And the clinic needs to be a member of the Ontario Veterinary Medical Association (OVMA).

Similar organizations and other subsidy programs exist across Canada. To find out if there’s one near you, contact your local Humane Society, SPCA groups, rescue groups, and veterinary medical associations. Many of these programs are region-specific and typically require a vet to submit the paperwork.

For example, my local Winnipeg Humane Society (WHS) offers low-cost vet care for pets with urgent medical needs. It is reserved for people who cannot afford care at their own clinic, and you have to call WHS to see if you qualify.

Budget-Saving Advice From a Veterinarian

“Euthanasia of a beloved pet is one of the worst parts of my job,” says Dr. Deborah Kelly, a vet with over 10 years of experience. “Having to make that decision based on cost alone is especially devastating, both for owners and for veterinary staff.”

Her biggest money-saving tip is pet insurance, ideally bought at the puppy/kitten stage. That’s when coverage is easiest to qualify for and less likely to come with exclusions for pre-existing conditions.

She said many plans include a short introductory free coverage period, often 4–6 weeks. “The cost of vet care has skyrocketed,” she said, largely due to advances in diagnostic technology and treatment options. Dr. Kelly has seen insurance prevent countless cost-driven euthanasias. She often recommends Trupanion because it allows direct billing. Other popular insurance providers include Petline, Petsecure, and OVMA Pet Health Insurance.

No, clinics don’t get paid to promote insurance. “The most ‘kickback’ I’ve ever gotten was some free pens,” she laughed.

Her most important piece of advice is to research breeds before choosing a pet, because some come with predictable, expensive health issues. She flagged brachycephalic (flat-faced) breeds as especially prone to breathing problems, skin infections, allergies, and back/vertebra injuries.

Remember Jack, the Bichon-Shih Tzu with the broken back? He was a brachycephalic breed and was put down because his owner couldn’t afford surgery.

Dr. Kelly also pointed to French Bulldogs, which often need airway corrective surgery that can run upwards of $3,000. And Labrador Retrievers are notorious for needing orthopedic or foreign-body extraction surgeries, which can land in the $3,000 to $7,000 range.

What I Learned After Calling 20 Vet Clinics

I had a feeling in-house payment plans would be super rare. But I was surprised to discover how many third-party finance options were available to fill the gap. And even more surprised to discover subsidy programs for low-income pet owners.

Of course, each option has its pros and cons. Credit cards are fast and easy. But rates are high, and interest gets expensive if you can’t pay off the balance. Financing gives you more wiggle room with longer terms and potentially lower rates. But that comes with applications, credit checks, and you’re restricted to in-network vet clinics.

Pet insurance can prevent debt entirely, but it comes with monthly premiums. Plus, it’s most helpful if you get it early, when your pet is young with no pre-existing conditions.

The smartest move is to plan before there’s an emergency. Start a pet-specific savings account. Choose an appropriate breed for your budget. Then call local clinics to ask what financing options they offer, and keep a short list of vets with accessible financing.